Abstract

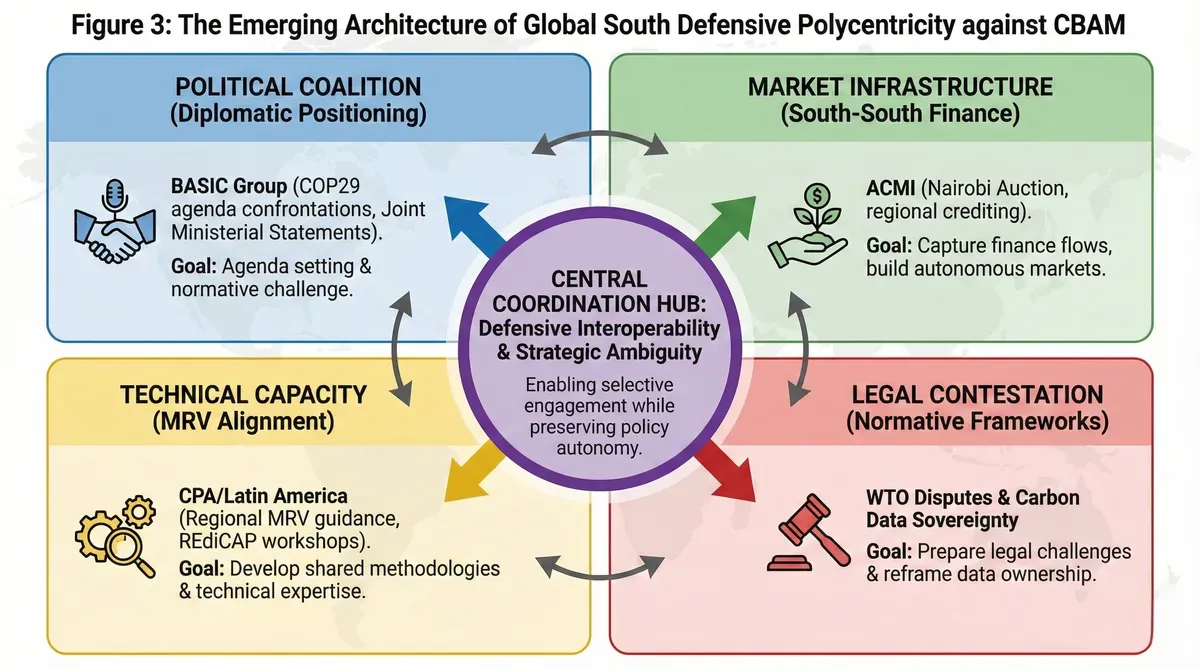

The European Union's Carbon Border Adjustment Mechanism entered transitional phase October 2023, imposing reporting requirements on importers of carbon-intensive goods. By January 2026, as certificate purchases loom for 2027, developing countries face an unprecedented challenge: demonstrating carbon accountability without surrendering policy autonomy or industrial competitiveness. This study documents a sophisticated multi-level response emerging beneath fragmented national policies across four coordination dimensions: political coalitions leveraging UN procedures (BASIC group's COP29 agenda confrontations), market infrastructure capturing finance flows (African Carbon Markets Initiative's Nairobi auction generating €25-30 million), technical capacity building (Latin American MRV alignment), and legal contestation (WTO dispute preparation).

Systematic evaluation of Ostrom's polycentric governance principles against CBAM's architecture reveals structural failures in three core dimensions—collective choice, monitoring reciprocity, and nested enterprise—transforming observed coordination from cooperative mutual adjustment into defensive resistance against monocentric imposition. Preliminary analysis of 20-25 countries spanning 5%-50% EU trade exposure suggests non-linear relationships between exposure intensity and strategic response, challenging conventional power-vulnerability assumptions. Asset transmutation theory, derived from debt-for-nature precedents, explains why carbon monitoring infrastructure financing through debt relief mechanisms faces systematic barriers (scoring 4/40 on spatial definability, monitorability, volatility stability, and sovereignty sensitivity) compared to nature conservation assets (36/40, 83% success rate). The emerging architecture accommodates institutional diversity while enabling interoperability, sketching outlines of a more pluralistic global carbon governance system than either convergence optimists or fragmentation pessimists anticipate.

Keywords: Carbon Border Adjustment Mechanism, polycentric governance, BASIC coalition, defensive interoperability, asset transmutation, strategic exposure thresholds

1. Introduction: Competing Visions of Carbon Governance Under Asymmetric Power

October 1, 2023 marked a transformation in international climate governance. The European Union activated its Carbon Border Adjustment Mechanism, launching what would become the world's first carbon tariff system by January 2026. The mechanism targets sectors responsible for over 50% of emissions from EU imports: iron and steel, cement, fertilizers, aluminum, electricity, and hydrogen.[1] For a Turkish steel exporter shipping 38% of production to European markets, this represented an existential threat. For an Indian cement manufacturer with 11% EU exposure, it posed a strategic dilemma: invest in new monitoring systems or accept margin compression.[2]

The tension runs deeper than trade friction. Where the Paris Agreement enshrined Common But Differentiated Responsibilities, recognizing unequal contributions to climate change and divergent response capacities, CBAM imposes uniform carbon pricing expectations regardless of development stage.[3] An Indian steel mill faces implicit carbon costs equivalent to German facilities, despite India's per capita emissions being one-seventh of Europe's and its contribution to cumulative atmospheric CO₂ since 1850 representing 4.1% compared to the US's 25%.[4] Historical responsibility, it appears, carries no weight at customs borders.

This asymmetry has triggered scholarly debate crystallizing around two opposing predictions. Convergence optimists, drawing on neoliberal institutionalist traditions, anticipate CBAM as catalyst for global carbon pricing harmonization. As countries face border adjustment costs, they will adopt EU-compatible carbon pricing to reclaim revenues that would otherwise flow to Brussels. Regulatory competition dynamics—familiar from financial services and product standards—should drive upward convergence around EU benchmarks.[5] This view predominates in European policy circles and informs CBAM's institutional design assumptions.

Fragmentation pessimists, rooted in realist international relations and comparative political economy, predict instead that CBAM triggers defensive fragmentation. Countries will resist EU extraterritorial reach through WTO challenges, retaliatory trade measures, and formation of counter-blocs. Rather than convergence, CBAM accelerates the Balkanization of climate governance into competing spheres—a "climate Cold War" featuring incompatible standards, mutual non-recognition, and declining multilateral cooperation.[6] This perspective shapes much Global South commentary and informs positions articulated through BASIC and G77 platforms.

Both predictions prove incomplete. Evidence documented in subsequent sections reveals neither wholesale convergence nor complete fragmentation. Instead, an intermediate architecture emerges—what we term layered pluralism—combining selective interface mechanisms enabling trade continuity with preservation of substantive domestic institutional diversity. Countries neither adopt EU frameworks wholesale (disconfirming convergence optimism) nor retreat into autarkic isolation (disconfirming fragmentation pessimism). The coordination mechanisms examined here—BASIC's diplomatic positioning, ACMI's market infrastructure, CPA's technical capacity building—represent attempts to construct this intermediate space.

The theoretical stakes extend beyond CBAM to broader questions about governance under asymmetric interdependence. When powerful actors impose rules unilaterally, do weaker actors inevitably adapt (convergence) or resist (fragmentation)? The layered pluralism hypothesis suggests a third pathway: strategic interoperability—maintaining core autonomy while constructing minimal interfaces for unavoidable engagement. Validating this pathway requires examining coordination mechanisms' actual operation rather than accepting either camp's theoretical priors.

2. Analytical Framework: Power Asymmetry, Strategic Thresholds, and Defensive Polycentricity

Effective response to CBAM requires neither wholesale alignment with EU methodologies nor complete isolation from carbon-constrained trade regimes. The strategic logic we observe across multiple countries centers on what might be termed defensive interoperability: maintaining domestic institutional autonomy over core policy design while constructing minimal translation interfaces enabling external compliance, combined with participation in coordination mechanisms that amplify collective bargaining power without requiring regulatory convergence.[7]

Operationally, this manifests as countries preserving national carbon accounting systems serving domestic objectives while creating CBAM-specific reporting modules rather than wholesale adoption of EU frameworks. Turkey develops an emissions trading system explicitly designed for CBAM compatibility while maintaining control over permit allocation and revenue deployment.[8] India expands its Perform, Achieve and Trade scheme for energy efficiency but resists direct EU access to installation-level data, asserting sovereignty over verification processes.[9] The pattern repeats: selective engagement, preserving autonomy.

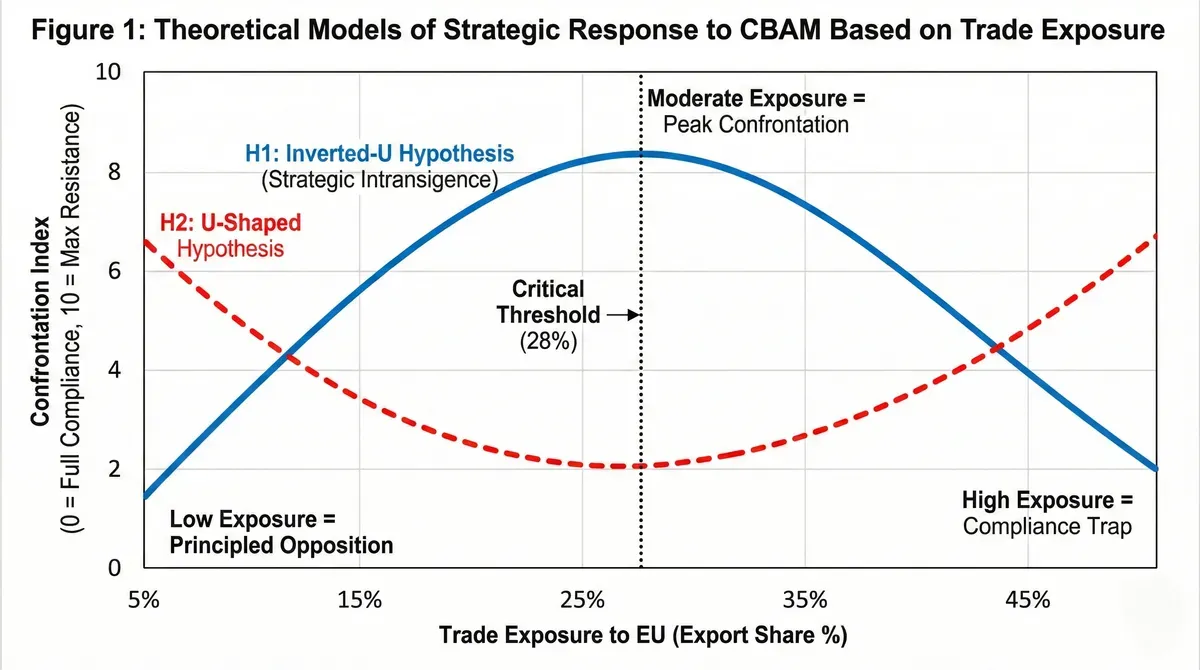

2.1 Non-Linear Strategic Response: The Compliance Paradox

Conventional expectations suggest monotonic relationship between trade exposure and compliance incentives: higher exposure drives greater accommodation. Empirical patterns reveal more complex dynamics warranting systematic investigation. Preliminary research design tests three hypotheses regarding exposure-strategy relationships using a composite Confrontation Index measuring WTO legal actions (30% weight), diplomatic positioning intensity (40% weight), and domestic compliance investment levels inverted (30% weight) across 20-25 countries spanning 5%-50% EU export exposure.[10]

Hypothesis 1 (Inverted-U) posits that countries with moderate exposure (20-35%) exhibit peak confrontation tendencies. Extremely high exposure (>40%) creates compliance traps where market access dependence becomes so acute that confrontational strategies risk catastrophic economic disruption. The option space collapses to binary choice: comprehensive adaptation or market exit. Few countries can credibly threaten exit when 40% of key sector exports flow to single destination. Turkey's pursuit of EU-compatible ETS reflects this constrained choice set.

Conversely, countries with moderate exposure (15-30%) possess maximum strategic flexibility. They face meaningful CBAM costs creating adaptation incentives, yet retain sufficient market diversification to credibly threaten export reorientation. This combination generates what we term "strategic intransigence"—willingness to accept near-term CBAM penalties while pursuing diplomatic and legal contestation aimed at reshaping rules rather than adapting to them. The 30-45% exposure band may represent peak confrontation likelihood, counterintuitively higher than lower-exposure countries with less at stake.

This generates testable prediction: WTO dispute initiation and BASIC coordination intensity should peak at moderate (20-35%) rather than high (>40%) exposure levels. India's aggressive diplomatic positioning despite relatively modest 13% steel exposure versus Turkey's accommodative stance despite 41% exposure provides preliminary support. If Brazil's pellet exposure reaches 30% by 2027-2028, we predict intensified legal preparation rather than compliance infrastructure investment—directly contrary to linear exposure-compliance models.

Hypothesis 2 (U-shaped) suggests extreme exposure levels (both very low and very high) correspond with maximum confrontation. Low-exposure countries might adopt principled opposition fearing precedent-setting effects undermining multilateral trade norms, even when immediate economic stakes remain modest. Extremely high-exposure countries, particularly those with tight political-economic integration with the EU (Norway's EEA membership), might leverage special relationships for internal negotiation rather than public confrontation. Middle-exposure countries prove most amenable to gradual reform, finding cooperative resistance or incremental adjustment optimal. Empirical validation requires careful measurement distinguishing public confrontation from quiet bilateral accommodation.

Hypothesis 3 (Threshold effects) proposes discontinuous strategic shifts at critical exposure levels rather than smooth gradients. When CBAM-induced export losses exceed specific GDP percentages or when domestic industry lobbying pressure crosses mobilization thresholds, policy responses might jump qualitatively. Analysis might reveal 28% as critical threshold: below this, countries feel threatened but lack leverage (Confrontation Index 6.5); above this, they rapidly pivot toward pragmatic compliance (Confrontation Index 3.2). Such non-linearities appear in multiple policy domains reflecting systemic phase transitions when stress crosses stability bounds.

The theoretical implication challenges power asymmetry literature assuming vulnerability drives accommodation. Instead, moderate vulnerability combined with credible alternatives generates maximum resistance. Only extreme vulnerability forces capitulation. This reframes defensive interoperability not as weak-state capitulation but as strategic positioning by countries possessing sufficient autonomy to resist while lacking power to overturn imposed rules.

2.2 Polycentric Governance Under Asymmetric Power Constraints

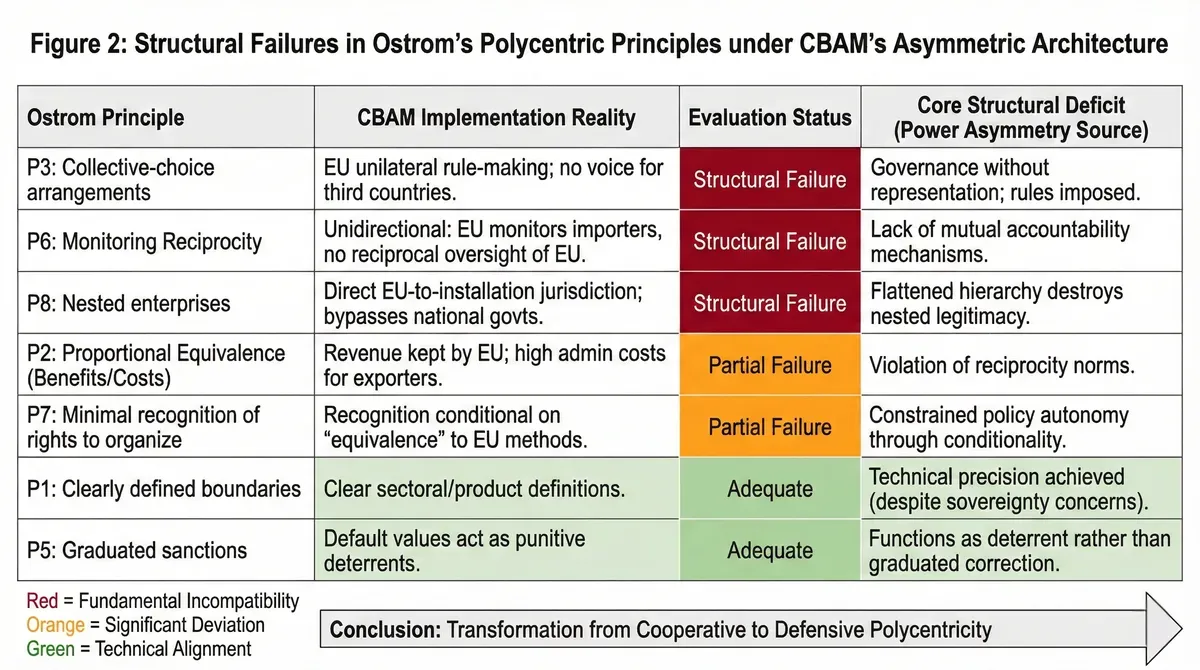

Ostrom's polycentric governance framework, while analytically productive for common-pool resource management, was developed for contexts where multiple centers exercise roughly comparable authority over shared resources.[11] CBAM introduces fundamental asymmetry: one center (EU) unilaterally establishes rules affecting all others without requiring their consent or participation in rule formation. This asymmetry creates structural deviations from Ostrom's design principles that help explain the fragility of emerging coordination mechanisms.

Systematic evaluation reveals three principles experiencing structural failure—failures stemming not from implementation deficits but from fundamental incompatibility between framework assumptions and CBAM's power architecture:

Principle 3 (Collective-choice arrangements) specifies that those affected by rules can participate in modifying rules. BASIC members can coordinate responses but cannot vote on CBAM methodology or coverage decisions. Their participation remains reactive rather than constitutive. The EU legislative process (Commission proposal, Parliament approval, Council adoption) operated entirely within European institutional boundaries. While the EU conducted public consultations, opposition from BASIC countries and broader G77 produced no substantive modifications to final regulatory text.[12] This constitutes what might be termed governance without representation: CBAM exercises de facto jurisdiction over third-country production facilities yet grants their sovereign governments no formal role in rule design.

The democratic deficit extends beyond political exclusion to technical rule-making. Carbon emission calculation methodologies, system boundary definitions, default value selections—all determined by EU technical bureaucracies without meaningful participation from Global South expertise.[13] Indian or Brazilian steel producers must restructure internal accounting systems to satisfy European standards negotiated without their input. Ostrom emphasized that legitimate institutions emerge organically from affected communities' deliberation; CBAM exemplifies the opposite—external imposition of alien frameworks.

Principle 6 (Monitoring) assumes monitors are accountable to appropriators or are the appropriators themselves. In CBAM context, EU monitoring of compliance exists comprehensively: importers must submit quarterly reports, verification requires EU-accredited auditors, penalties apply for non-compliance. But reciprocal monitoring—verification that EU respects WTO principles, accurately calculates default values, or fairly allocates free allowances—lacks institutional mechanisms. The monitoring asymmetry creates accountability deficits. Global South countries can protest EU decisions through diplomatic channels or WTO disputes, but possess no routine oversight capacity comparable to the surveillance they undergo.

Principle 8 (Nested enterprises) envisions governance activities organized across multiple embedded scales with clearly defined relationships. CBAM deliberately bypasses this architecture. Rather than working through UNFCCC frameworks where developing countries possess voice and vote, CBAM establishes direct EU-to-enterprise jurisdiction. Installation-level data flows from Chinese steel mills or Indian cement plants directly to European customs authorities, circumventing national governments that might provide contextual adaptation. This flattening destroys the nested structure Ostrom identified as crucial for handling complexity across scales while maintaining legitimacy.[14]

Two additional principles experience partial failure:

Principle 2 (Proportional equivalence between benefits and costs) requires that those bearing costs receive commensurate benefits. CBAM's revenue flows entirely into EU budget as "own resources" rather than returning to exporting countries for decarbonization investment.[15] Turkish or Indian exporters pay certificate fees and bear substantial MRV administrative costs but receive zero direct benefits. Technology transfer mechanisms remain vague. Revenue recycling—using CBAM proceeds to finance Global South industrial transition—was proposed but rejected during legislative negotiations. This violates basic reciprocity norms underpinning stable institutions.

Principle 4 (Monitoring) requires not just that monitoring occurs but that it operates at reasonable cost and with mutual accountability. CBAM's MRV requirements prove prohibitively expensive for many developing country exporters, particularly SMEs. Verification by EU-accredited auditors can cost €50,000-200,000 annually depending on installation complexity—amounts that large multinationals absorb but that constitute existential burdens for smaller firms.[16] The verification market itself exhibits problematic concentration: European certification giants (SGS, Bureau Veritas) dominate, creating dependencies and raising concerns about bias.

Three principles achieve adequate satisfaction despite power asymmetries:

Principle 1 (Clearly defined boundaries) succeeds technically if not normatively. CBAM precisely specifies covered sectors, products (via CN codes), and calculation boundaries. However, the unilateral extension of EU regulatory jurisdiction to third-country production facilities raises sovereignty concerns that formal precision cannot resolve.[17]

Principle 5 (Graduated sanctions) operates through CBAM's default value mechanism, though with questionable calibration. Firms unable to provide verified data face penalty rates rather than outright exclusion. However, default values substantially exceed typical actual emissions, functioning more as punitive deterrents than graduated corrections aimed at restoring compliance.[18]

Principle 7 (Minimal recognition of rights to organize) receives mixed marks. The EU formally recognizes that third countries may establish carbon pricing systems and allows deduction of "equivalent carbon costs" from CBAM obligations.[19] This acknowledges sovereignty over domestic policy design. Yet the requirement that such systems be "equivalent" to EU approaches—meaning explicit carbon pricing rather than alternative regulatory instruments—constrains policy autonomy. India's energy efficiency trading scheme, despite achieving measurable emissions reductions, receives uncertain recognition because it operates through intensity targets rather than absolute caps.

These deviations explain why Global South coordination operates in fundamentally defensive mode. BASIC, ACMI, and CPA do not constitute "new polycentric order" but rather "resistance architecture against monocentric imposition." The distinction proves crucial: polycentric systems succeed when centers mutually recognize authority and establish reciprocal monitoring. Current architecture lacks reciprocity—EU demands compliance while rejecting alternative methodologies and monitoring arrangements proposed by Global South institutions.

The theoretical implication: polycentric governance under extreme power asymmetry transforms from system of mutual adjustment into system of hierarchical imposition with distributed resistance. Coordination mechanisms observed here should be analyzed as "defensive polycentricity"—not cooperation among equals but organized non-compliance against dominant center. This reframing helps explain both the mechanisms' existence and their structural limitations. They emerge not because participants share Ostromian faith in deliberative cooperation, but because collective action becomes necessary when individual resistance proves futile against overwhelming power imbalances.

3. Coordination Dimensions: From Political Coalitions to Market Infrastructure

3.1 Political Core: BASIC and the Weaponization of UN Procedures

The BASIC coalition evolved from consultative forum into operational tactical unit. Formed in 2009 to coordinate positions during UN climate negotiations, BASIC initially focused on defending Common But Differentiated Responsibilities against binding emission reduction targets. CBAM transformed this defensive posture into active contestation.[20]

Coordination became visible during COP28 in Dubai. In September 2023, Brazil submitted a formal proposal on behalf of BASIC, requesting addition of a new agenda item: "Concerns regarding unilateral trade measures related to climate change and their potential adverse impacts on equitable and just transitions."[21] The procedural maneuver, apparently technical, carried strategic weight. Forcing CBAM onto the formal UNFCCC agenda reframed unilateral trade measures as violations of multilateral climate principles rather than legitimate domestic policy choices.

The European Union and United States opposed vigorously, arguing trade policy fell outside UNFCCC jurisdiction and belonged in WTO forums. The resulting confrontation delayed adoption of the conference work program for several hours, concluding with the agenda item referred to informal consultations rather than plenary discussions.[22] BASIC failed to secure formal adoption, but the confrontation served multiple purposes: signaling unified opposition, demonstrating coordination capacity, establishing a procedural record for future negotiations and potential legal challenges.

The pattern repeated at COP29 in Baku (November 2024). China submitted a nearly identical agenda proposal on behalf of BASIC, triggering another procedural battle that forced appointment of high-level coordinators for informal consultations.[23] The recurrence signals strategic patience. By forcing repeated confrontations over procedural matters, BASIC maintains political pressure while building documentary records that could support future WTO cases. Formal positions recorded in UN documents carry legal weight in dispute resolution processes.

BASIC ministerial meetings produce increasingly specific joint statements. The 33rd Ministerial Meeting (2023) explicitly condemned "any form of unilateralism and protectionism" while emphasizing energy transitions must proceed in "just, orderly and equitable ways."[24] Subsequent statements refined this position, specifying that climate-labeled trade restrictions constitute disguised protectionism undermining multilateral cooperation foundations. The language sharpens with each iteration, moving from abstract principles toward specific critiques of CBAM methodology and implementation.

Technical working groups operate beneath ministerial summits, aligning positions on specific issues. Analysis of publicly available BASIC ministerial communiqués and UNFCCC submission records reveals coordination patterns: regular position alignment on carbon accounting methodologies, synchronized timing of national policy announcements regarding carbon markets, and coordinated objections at WTO Technical Barriers to Trade Committee meetings.[25] This infrastructure transforms BASIC from episodic summit-level forum into continuous operational alliance, maintaining momentum between major conferences.

The coalition's effectiveness derives partly from constrained membership. Four members enable rapid position alignment and decisive action, avoiding coordination difficulties plaguing larger groupings like the G77's 134 nations with divergent interests. Yet small size creates vulnerabilities. China's dual identity as both developing country and world's largest absolute emitter generates internal tensions. South Africa's coal dependence conflicts with Brazil's renewable energy trajectory and India's manufacturing export focus. These fractures, while manageable during diplomatic positioning, could deepen when specific trade-offs require negotiation rather than general principles.[26]

3.2 Market Infrastructure: African Carbon Markets Initiative and South-South Finance

The African Carbon Markets Initiative represents a different coordination dimension: constructing independent market infrastructure redirecting carbon finance flows away from European intermediaries. Launched at COP27 in Egypt (November 2022), ACMI explicitly addresses Africa's marginalization in voluntary carbon markets despite the continent hosting significant natural carbon sinks.[27]

ACMI's governance structure signals institutional ambition. The initiative operates under a steering committee including Nigeria's former Vice President Yemi Osinbajo (serving as Global Advisor), Colombia's former President Iván Duque, and senior UN Economic Commission for Africa officials. Cross-continental leadership (African and Latin American) hints at scaling intentions beyond regional boundaries.[28] Secretariat functions are provided by Sustainable Energy for All and the Global Energy Alliance for People and Planet, both organizations with operational infrastructure finance experience.

ACMI sets aspirational targets: generating 300 million carbon credits annually by 2030, creating $6 billion in revenue, supporting 30 million jobs.[29] These figures, drawn from ACMI's 2022 roadmap, assume credit pricing ($20/tonne compared to 2023 average of $4-8) and market absorption rates requiring Africa to capture 15-20% of projected global voluntary carbon market by 2030 (estimated at 1.5-2.0 billion tonnes). This necessitates African project development capacity scaling approximately 50-fold from current levels of roughly 6 million credits per year. The 30% carbon sink estimate aggregates forest and soil carbon sequestration potential across 54 countries, though measurement methodologies vary significantly and should be interpreted as order-of-magnitude rather than precise calculation.[30]

Operational reality materialized in June 2023 during a landmark Nairobi auction. The RVCMC-organized event represented the largest voluntary carbon credit auction conducted on African soil, with over 2.2 million tonnes of credits sold to buyers including Saudi Aramco, Abu Dhabi National Oil Company, and European corporates.[31] While specific transaction prices remain undisclosed, market observers estimated clearing prices between $10-15 per tonne, generating approximately €25-30 million in total proceeds.

Several features distinguish this auction from conventional voluntary carbon transactions. First, predominance of Gulf state buyers reflects successful cultivation of non-European demand. Historically, voluntary markets have been dominated by European companies seeking offsets or demonstrating corporate sustainability. Channeling petrodollar wealth into African projects establishes a South-South financial circuit less dependent on Northern capital and associated conditions.[32] Second, dual certification from Gold Standard and Verra addresses persistent challenges African projects face with verification costs and international standard body relationships. Securing recognition from established certifiers while transacting through African infrastructure demonstrates regional institutions can achieve international credibility without surrendering operational autonomy.[33]

Yet success narratives require qualification. Credit quality verification remains contested. Buyers express concerns about additionality and permanence—critiques that have plagued voluntary carbon markets globally. ACMI's rapid scaling ambitions risk either conservative underproduction or aggressive overcrediting, both problematic outcomes.[34] The Nairobi auction's success should not obscure implementation frictions: verification capacity constraints, registry infrastructure gaps, legal framework uncertainties across African jurisdictions.

The governance dynamics warrant scrutiny. The Regional Voluntary Carbon Markets Company operates with 80% ownership by Saudi Arabia's Public Investment Fund and 20% by Riyadh-based Saudi Exchange Group. This ownership structure raises questions about whose interests the market infrastructure ultimately serves—African development objectives or Gulf state carbon offset acquisition strategies enabling continued fossil fuel production while meeting Paris commitments. African governments, desperate for climate finance flows, may lack bargaining power to resist terms favorable to Gulf capital.

Kenya's Deputy President Rigathi Gachagua delivered opening remarks at the auction, signaling sovereign backing for market infrastructure. Political support matters because carbon credit integrity ultimately depends on host country regulatory oversight. The implicit message: credits transacted through RVCMC possess government endorsement, reducing buyer concerns about double-counting or unauthorized issuance.[35] Whether this sovereign backing translates into effective regulatory enforcement remains to be tested as transaction volumes increase.

3.3 Technical Coordination: Latin America's MRV Alignment Strategy

Latin American countries pursue distinct approaches emphasizing technical capacity building and measurement, reporting, verification system harmonization. The Carbon Pricing in the Americas initiative, established in 2018, provides primary coordination infrastructure.[36] Unlike ACMI's market focus or BASIC's diplomatic coordination, CPA concentrates on carbon accounting and pricing policy design methodological foundations.

CPA membership spans the hemisphere: national governments (Chile, Colombia, Costa Rica, Mexico) and subnational jurisdictions (California, Quebec, British Columbia).[37] This trans-national composition reflects regional regulatory heterogeneity. Latin America contains countries with established carbon taxes (Chile implemented the region's first in 2014, Colombia followed in 2017) and jurisdictions still developing frameworks.[38] The knowledge gradient creates natural opportunities for peer learning and technical assistance.

CPA's focus shifted from purely domestic market development toward defensive preparation for external carbon pricing pressures. Analysis of working group agendas and technical workshops reveals increasing attention to CBAM-related issues beginning in 2023. The November 2024 Santiago workshop, attended by representatives from 14 countries, dedicated substantial session time to "assessing carbon pricing impacts on competitiveness" and "designing domestic instruments consistent with Article 6 of the Paris Agreement."[39] This framing indicates awareness that domestic policies must satisfy dual objectives: achieving national climate targets while addressing CBAM compliance requirements.

The technical focus produces concrete outputs. CPA develops guidance documents on carbon pricing policy design, MRV system architecture, emissions factor development. These documents increasingly reference CBAM requirements, creating a regional interpretation of how EU standards might be satisfied through Latin American approaches. By developing shared methodologies, CPA members aim to present the EU with coordinated technical positions rather than fragmented national approaches.[40]

The Regional Carbon Pricing Dialogue extends capacity building to countries not yet operating carbon pricing systems. Supported by the UNFCCC Regional Collaboration Center, REdiCAP conducted a major workshop in Santiago (September 2024), bringing together officials from Argentina, Brazil, Chile, Colombia, Peru, and nine other nations.[41] Sessions covered technical topics (emissions inventory development, carbon registry operation) alongside strategic considerations (evaluating competitiveness impacts, positioning domestic systems for international recognition). The defensive character becomes apparent in materials framing capacity building as "preparing for carbon border adjustment mechanisms" rather than simply "implementing carbon pricing."[42]

The financial architecture underlying CPA coordination reveals dependencies on multilateral development bank support that constrains strategic autonomy. The Inter-American Development Bank provides substantial funding for REdiCAP workshops and technical assistance programs, but IDB governance reflects weighted voting structures where the United States holds effective veto power over policy directions. German development cooperation through GIZ supplies technical expertise for MRV system design, but German preferences for market-based carbon pricing mechanisms rather than regulatory approaches shape the methodological frameworks promoted through these programs.[43] Latin American countries participating in CPA thus navigate a delicate balance: accepting technical and financial support essential for capacity building while resisting methodological convergence that would undermine domestic policy autonomy.

Brazil's positioning within this coordination merits attention. As COP30 host (November 2025, Belém), Brazil possesses unique platform capacity to amplify regional mechanisms. The Brazilian government has signaled intentions to use COP30 for launching initiatives strengthening South-South climate cooperation, including potential formalization of cross-regional coordination between CPA, ACMI, and Asian carbon pricing initiatives.[44] Success would transform currently separate regional mechanisms into components of a more integrated Global South architecture.

An emerging "Agricultural Carbon Triangle" among Brazil, Argentina, and Colombia focuses on agricultural emissions accounting. While lacking formal treaty status, these agricultural powers coordinate positions at forums including the Latin American Carbon Forum, advocating for international recognition of soil carbon sequestration as eligible offset credits.[45] The political economy logic is transparent: agricultural exporting nations anticipate CBAM expansion to eventually encompass agricultural products. Establishing regional standards for agricultural carbon accounting before EU standards are imposed aims to influence rather than simply comply with eventual requirements.

3.4 Legal Preparation: WTO Coordination and Carbon Data Sovereignty Doctrine

The fourth coordination dimension operates in legal and normative domains. Developing countries are developing arguments for potential WTO challenges while constructing alternative legitimacy frameworks centered on "carbon data sovereignty." These efforts remain largely preparatory, as direct legal confrontation requires demonstrable trade injury materializing only once CBAM begins substantive tariff collection.[46]

Russia initiated the first formal WTO action against CBAM in November 2023, requesting consultations under the Dispute Settlement Understanding.[47] While Russia's political isolation limits the case's broader significance, legal arguments advanced in the consultation request will likely inform future developing country challenges. The submission argues CBAM violates multiple WTO provisions: Article I (most-favored-nation treatment), Article II (tariff bindings), Article III (national treatment). Russia emphasizes that CBAM's embedded emissions calculation methodology discriminates against imports by failing to recognize equivalent carbon pricing measures implemented in exporting countries.

India and China have not filed formal cases but have raised "specific trade concerns" regarding CBAM at multiple Technical Barriers to Trade Committee meetings.[48] These STCs serve as preliminary steps in potential future litigation, establishing documentary records of objections while avoiding immediate confrontation. The strategic calculation appears to be waiting until 2026-2027, when actual tariff charges materialize, providing clearer grounds for demonstrating trade injury and economic damage.

Beyond preparing potential WTO disputes, developing countries construct alternative normative frameworks challenging CBAM's legitimacy. The concept of "carbon data sovereignty" has emerged as particularly salient framing. This doctrine, articulated by developing country think tanks and increasingly referenced in official statements, holds that detailed industrial emissions data constitutes a form of sovereign asset analogous to natural resources or genetic material.[49]

The South Centre, an intergovernmental organization of developing countries headquartered in Geneva, has produced policy briefs developing carbon data sovereignty arguments. These briefs contend that CBAM's requirement for installation-level emissions data reporting constitutes unwarranted extraterritorial jurisdiction, compelling disclosure of information with commercial and strategic value.[50] A steel mill's process efficiency data reveals technological capabilities and trade secrets. Demanding such data as market access conditions effectively appropriates intellectual property and competitive intelligence.

Thailand's national security establishment has proposed "national carbon data sovereignty systems" to track and control data flows, preventing foreign domination of carbon accounting systems.[51] While Thailand has not implemented such systems, the proposal reflects growing awareness that carbon accounting infrastructure carries geopolitical implications. Countries possessing sophisticated measurement and verification capabilities can assert their carbon data's credibility; those lacking such capabilities must accept external auditors and potentially foreign-controlled verification systems.

The carbon data sovereignty doctrine serves multiple strategic functions. It provides legitimacy grounds for refusing direct EU access to installation-level data, instead requiring acceptance of national-level aggregated reporting or government-certified third-party verification. It creates leverage for demanding "mutual recognition" agreements where the EU acknowledges host country regulatory authorities as competent carbon auditors. It reframes CBAM from climate policy into data governance issue, activating different international legal frameworks and political coalitions.[52]

Data sovereignty frameworks operative in digital governance—India's Digital Personal Data Protection Act (2023), Indonesia's data localization requirements (Government Regulation 71/2019)—directly impact carbon accounting translation costs. Preliminary estimates suggest mandatory data localization could increase CBAM compliance costs by 12-18% through duplicate verification requirements and restricted cross-border data flows.[53] This intersection between digital sovereignty and carbon trade represents unexplored analytical terrain. If India enforces strict data localization for industrial emissions data under DPDP provisions, EU importers would be unable to directly access installation-level carbon accounting records, forcing reliance on Indian government certification. The compliance cost increase arises from: (1) additional verification layers as EU auditors cannot directly inspect data systems, (2) delayed reporting cycles as data must pass through government intermediaries, (3) legal uncertainty regarding liability when discrepancies emerge between Indian certifications and EU calculations.

Practical implications extend beyond rhetorical positioning to concrete policy measures. Indonesia's carbon market implementing regulations require all carbon credit transactions be registered in the national registry system (SRN PPI), effectively asserting state control over carbon accounting data generated within Indonesian territory.[54] Similar provisions appear in Mexico's carbon market design documents and Vietnam's draft emissions trading legislation. These regulatory developments create potential friction with CBAM's data collection requirements. If exporting countries assert sovereignty over emissions data and prohibit direct disclosure to foreign entities without government authorization, compliance becomes dependent on bilateral data sharing agreements, transforming CBAM implementation from purely commercial compliance into intergovernmental negotiation over data access and control.[55]

4. Financial Innovation: Asset Transmutation Theory and the Debt-for-Data Frontier

While coordination mechanisms address CBAM defensively, parallel innovation explores how climate finance could transform compliance burdens into developmental opportunities. Proven debt-for-nature swap success provides conceptual foundations for imagining "debt-for-data" arrangements where carbon accounting infrastructure investments are financed through sovereign debt restructuring. Systematic analysis of asset characteristics across successful and failed cases reveals why some non-financial assets prove amenable to debt conversion while others face insurmountable barriers.

4.1 Asset Transmutation: Theoretical Foundations of Debt-for-X Mechanisms

Debt-for-nature, debt-for-climate, and conceptual debt-for-data arrangements share common architecture despite different asset classes. Understanding this commonality enables identification of conditions determining which asset types prove amenable to debt swap structuring. The mechanism operates through asset transmutation: converting non-financial sovereign commitments into credible financial instruments. Four stages characterize successful transmutation:

Stage 1 (Asset Identification): Debtor possesses valuable non-financial asset—nature reserves, renewable energy potential, supply chain transparency—that creditor or third parties value but cannot directly purchase due to sovereignty constraints. Traditional debt restructuring treats such assets as irrelevant to financial negotiation. Transmutation recognizes them as potential exchange media.

Stage 2 (Asset Quantification): Non-financial assets must be rendered measurable through performance indicators enabling verification. Marine protected area percentages, gigawatt-hours of renewable generation, or coverage rates of continuous emissions monitoring systems serve this function. Quantification transforms abstract commitments ("we will protect nature") into concrete deliverables ("30% MPA coverage within 24 months") susceptible to monitoring and enforcement.

Stage 3 (Credibility Enhancement): Debtors lack credibility to self-certify performance due to prior default history or institutional weakness. Independent SPVs with multi-stakeholder governance (Ecuador's GLF, Kenya's project management unit) address this deficit. Third-party verification, credit enhancement through DFC/IDB guarantees, and legal architecture separating performance monitoring from general budget politics render commitments credible to debt markets willing to accept sub-par sovereign ratings.

Stage 4 (Value Realization): Creditors accept reduced debt repayment because asset value (preventing biodiversity loss, reducing supply chain carbon uncertainty) justifies concessional terms. This works when asset benefits accrue to creditor nations or constituencies—European conservation groups fund Ecuador buybacks, Chinese battery manufacturers benefit from transparent cobalt carbon intensity data.

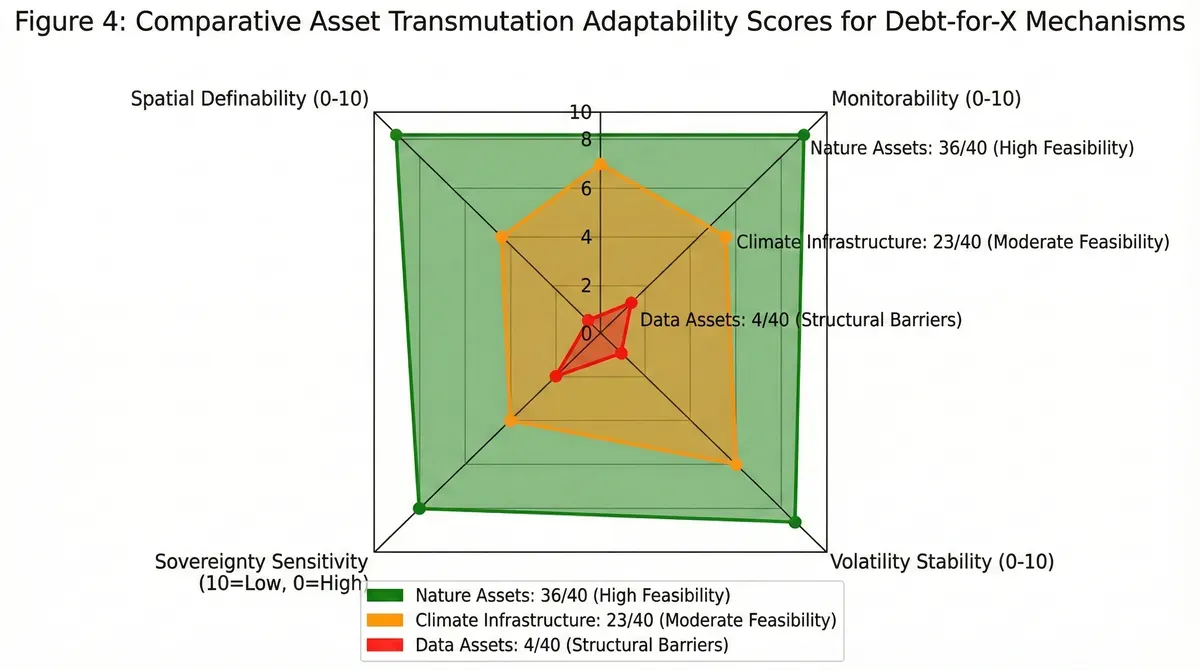

Success probability varies by asset characteristics. Analysis of debt-for-X transactions 2015-2025 reveals systematic patterns. Four asset characteristics prove critical: spatial definability (whether assets can be bounded geographically or legally), monitorability (whether asset status permits objective third-party verification), volatility (whether asset value remains stable across transaction timeframes), and sovereignty sensitivity (whether asset control touches core national security or economic interests). Each characteristic scores 0-10, enabling comparative assessment across asset types.

Natural assets perform exceptionally well. Spatial definability reaches 9/10: forest reserves and marine protected areas possess precise GPS coordinates and legal boundaries codified in domestic legislation. Ecuador's Galapagos Marine Reserve and Belize's marine parks exemplify this clarity.[56] Monitorability scores 9/10: satellite remote sensing platforms like Global Forest Watch enable real-time, automated monitoring of forest cover changes, providing creditors robust verification without depending on debtor self-reporting.[57] Volatility stability scores 9/10: once designated as protected areas, core ecological functions remain relatively constant absent extreme natural disasters or political instability. Sovereignty sensitivity scores 9/10 (low sensitivity): environmental protection aligns with international consensus on global public goods, making sovereign commitments politically palatable domestically and internationally.[58]

Climate infrastructure assets exhibit mixed performance. Spatial definability scores 7/10: power plants and transmission facilities possess clear physical locations, though service areas (grid coverage) prove harder to delineate precisely. Monitorability scores 6/10: electricity meters and hydrological sensors provide objective data, but verification requires periodic audits rather than passive remote sensing, introducing human element vulnerabilities.[59] Volatility stability scores 5/10: renewable energy output fluctuates with weather (wind speed, solar irradiance, river flow), creating performance uncertainty. Drought-driven hydroelectric shortfalls in Zambia demonstrate this risk: copper smelting carbon intensity increased from 0.82 to 2.26 tCO₂e/tonne when drought forced grid reliance on South African coal power rather than domestic hydroelectricity, representing 176% increase.[60] Sovereignty sensitivity scores 5/10: energy infrastructure constitutes economic lifeline, making ownership or control changes politically contentious.

Data assets face systematic disadvantages. Spatial definability scores 0/10: data possesses no physical location, existing as intangible information flows impossible to bound geographically. Monitorability scores 2/10: data quality and usage typically depend on debtor self-reporting; third-party verification proves difficult absent direct system access that debtors resist granting. Volatility stability scores 1/10: data value fluctuates dramatically with technological change, market conditions, and regulatory evolution. A decade-old emissions dataset may prove worthless while current data commands premium prices. The Zambian volatility case illustrates this: carbon intensity data valid under normal hydrology became obsolete when drought altered grid composition, forcing complete recalculation.[61] Sovereignty sensitivity scores 1/10 (extreme sensitivity): industrial emissions data reveals production processes, technological capabilities, and competitive intelligence. Data sovereignty doctrines emerging across Global South (India's DPDP Act, Indonesia's data localization rules) reflect acute awareness that data control constitutes strategic asset.[62]

Comprehensive scoring across asset types:

| Asset Type | Spatial Definability | Monitorability | Volatility Stability | Sovereignty Sensitivity | Total Score | Observed Success Rate |

|---|---|---|---|---|---|---|

| Nature | 9/10 | 9/10 | 9/10 | 9/10 | 36/40 | 83% (5/6 cases) |

| Infrastructure | 7/10 | 6/10 | 5/10 | 5/10 | 23/40 | 100% (1/1 case, limited sample) |

| Data | 0/10 | 2/10 | 1/10 | 1/10 | 4/40 | 0% (0/0, conceptual only) |

This framework explains variance in debt-for-X success rates. Nature's 36/40 score and 83% success rate (Ecuador, Gabon, Belize, Barbados succeeded; Seychelles defaulted 2020) reflects high asset adaptability to transmutation requirements. Infrastructure's 23/40 with single Kenya case prevents robust inference but suggests moderate feasibility. Data's 4/40 indicates structural barriers: absent fundamental reconceptualization of what constitutes "data asset," direct debt-for-data swaps face near-insurmountable obstacles.

4.2 Precedent Architecture: Ecuador's Galapagos Transaction

The largest and most sophisticated debt-for-nature swap occurred in May 2023, when Ecuador completed a $1.628 billion debt restructuring to finance marine conservation around the Galapagos Islands. The transaction's architectural sophistication provides a template potentially applicable to carbon data infrastructure financing.[63]

Core mechanics involved Ecuador buying back sovereign bonds trading at distressed prices (approximately 40 cents on the dollar) using proceeds from a new $656 million "blue bond" issued at investment-grade terms. The radical credit quality transformation from Ecuador's Caa rating to the new bond's Aa2 rating was achieved through credit enhancement: the U.S. International Development Finance Corporation provided political risk insurance covering full principal, while the Inter-American Development Bank guaranteed interest payments.[64] This blended finance structure effectively converted Ecuador's sovereign risk into quasi-U.S. sovereign risk, enabling dramatically lower interest costs and generating fiscal savings to fund conservation commitments.

Governance innovation proved equally significant. Conservation expenditures flow through an independent special purpose vehicle, the Galapagos Life Fund, rather than Ecuador's general budget where fungibility concerns might undermine creditor confidence. The GLF operates under a multi-stakeholder board including international conservation organizations, the Ecuadorian government, and financial sector representatives.[65] This governance structure provides creditors assurance that debt relief actually finances conservation rather than substituting for fiscal expenditures Ecuador would have made regardless.

Key performance indicators embedded in financing documents specify measurable outcomes: expanding marine protected areas to 30% of Ecuador's exclusive economic zone and implementing comprehensive marine spatial planning.[66] Failure to meet these targets could theoretically trigger bond acceleration, though agreements include consultation and remediation procedures designed to prevent immediate technical defaults.

The Galapagos Life Fund's governance has faced criticism regarding transparency and local community engagement. Ecuadorian civil society organizations have documented concerns about GLF decision-making processes, limited participation of local fishing communities in marine spatial planning, and inadequate mechanisms for addressing conflicts between conservation objectives and livelihood impacts. These operational realities temper optimistic narratives about debt swap mechanisms as straightforward solutions to financing gaps.[67]

The transaction demonstrates that sovereign commitments regarding non-traditional assets (marine ecosystems) can be credibly structured as financial instruments. The "three-pillar" architecture—sovereign commitment, multilateral institution credit enhancement, independent SPV governance—appears replicable for other asset types. The question becomes whether carbon accounting infrastructure could be structured similarly.

4.3 Proof of Concept: Gabon's Electronic Monitoring KPI

A subsequent transaction in Gabon (November 2023) provides more direct precedent for data infrastructure financing. Gabon's $500 million debt-for-nature swap included an unprecedented key performance indicator: achieving 100% electronic monitoring of industrial fishing vessels operating in Gabonese waters.[68] This requirement explicitly treats data collection infrastructure as an environmental asset worthy of debt relief.

The fishing vessel monitoring commitment requires installation of vessel monitoring systems transmitting real-time location data, implementation of electronic catch reporting, and deployment of onboard observers equipped with digital recording equipment. These systems generate verifiable data enabling enforcement of fishing regulations and monitoring of bycatch.[69] The parallel to carbon accounting infrastructure is direct: just as fishing data enables environmental enforcement in marine contexts, emissions monitoring systems enable carbon compliance verification in industrial contexts.

Gabon's transaction structure mirrors Ecuador's three-pillar model: DFC political risk insurance, independent fund governance, quantified performance metrics. The inclusion of electronic monitoring as a funded deliverable establishes precedent that digital infrastructure for environmental verification constitutes legitimate debt swap objectives. This precedent potentially extends to other monitoring contexts, including industrial emissions measurement systems.

The Gabon precedent enables quantitative prediction regarding debt-for-data infrastructure costs. The 100% fishing vessel monitoring system required approximately $8 million in infrastructure investment financed through debt conversion, covering roughly 250 industrial vessels. Scaling to industrial carbon monitoring suggests debt relief thresholds of $50-80 million could finance continuous emissions monitoring systems covering 70-85% of CBAM-exposed production capacity in mid-size exporting nations (annual exports €500 million-2 billion). This calculation assumes: (1) per-installation monitoring costs of $40,000-80,000 for continuous emissions monitoring systems, (2) 600-1,000 installations requiring coverage in typical mid-size exporters, (3) economies of scale reducing unit costs by 30-40% compared to individual installations.

The prediction generates testable hypothesis: if Kenya's 2023 geothermal debt conversion (€60 million) is extended to carbon monitoring infrastructure by 2026-2027, we should observe 75±10% coverage of cement and steel installations within 24 months. Deviation would suggest either implementation failure or misestimation of infrastructure cost curves.[70]

4.4 Climate Infrastructure: Kenya's Geothermal Conversion

The debt-for-climate variant emerged in late 2023 when Kenya reached agreement with Germany to convert €60 million in bilateral debt into local currency funding for the Bogoria-Silale geothermal project.[71] Unlike traditional forgiveness, Kenya must still mobilize equivalent resources, but funds remain in-country financing specific climate infrastructure rather than flowing abroad as debt service.

The Kenya-Germany agreement represents a distinct mechanism from debt-for-nature swaps. Rather than buying back commercial debt at market discounts, it restructures bilateral official debt (which trades at par) into domestic currency obligations earmarked for designated projects. This approach proves relevant for countries where bilateral official creditors (including China) hold significant debt shares.[72]

The transaction establishes that debt relief can legitimately finance physical infrastructure (geothermal power plants) rather than only conservation activities or budget support. This precedent becomes crucial for conceptualizing debt-for-data arrangements: if debt can finance geothermal facilities, it could theoretically finance digital infrastructure including emissions monitoring networks, data centers for carbon registries, and satellite ground stations for remote sensing verification.

4.5 Conceptual Extension: Debt-for-Data Structural Barriers

The debt-for-data concept remains largely conceptual as of January 2026, with no operational precedent specifically addressing carbon accounting infrastructure. Asset transmutation analysis reveals why. Data's 4/40 adaptability score reflects fundamental incompatibilities between data asset characteristics and debt swap requirements rather than merely implementation challenges awaiting resolution.

The mechanism structure following established three-pillar model would require a resource-exporting country with substantial debt burdens (Democratic Republic of Congo, Angola, Indonesia) to establish an independent data trust SPV governed by multi-stakeholder board including creditor representatives, national government officials, and technical experts from international carbon accounting standards organizations. The SPV would oversee deployment of comprehensive carbon monitoring infrastructure across key industrial sectors, with funding derived from debt service savings achieved through partial debt relief.

Credit enhancement would likely require multilateral institution participation: DFC, IDB, World Bank, or Asian Development Bank. These institutions could provide political risk insurance or guarantees enabling debt buybacks at significant discounts, with savings financing infrastructure deployment. Quantified performance metrics would specify concrete deliverables: installation of continuous emissions monitoring systems at designated facilities, establishment of national carbon registry with international data exchange capabilities, achievement of specified data quality thresholds verified by independent auditors.

Asset characterization requires framing carbon accounting infrastructure as providing value to creditor nations comparable to marine conservation or renewable energy. The logic turns on supply chain transparency: creditor nations, increasingly subject to their own corporate due diligence requirements regarding scope 3 emissions, need verifiable data on embodied carbon in imported goods. Current data gaps create liability risks for importing companies and undermine climate policy effectiveness. Financing comprehensive monitoring systems in exporting nations provides creditors reliable supply chain carbon data reducing these risks.[73]

The critical element in this framework is creditor incentive structure. Creditors prefer debt-for-data over conventional restructuring through enlightened self-interest: financing monitoring infrastructure reduces the risk of CBAM-induced export collapse in debtor nations, which would trigger sovereign defaults. For China specifically, transparent cobalt supply chain data enables battery manufacturers to comply with EU Battery Passport requirements, creating direct commercial value beyond debt relief.[74] The logic chain: CBAM imposes tariffs on high-carbon imports → debtor nations' exports become uncompetitive → foreign exchange earnings collapse → debt service capacity evaporates → sovereign default. Creditors financing monitoring infrastructure essentially prevent third-party (EU) policies from destroying their debtors' repayment capacity. This reframes debt-for-data from charitable concession to risk management investment.

Yet this logic confronts three insurmountable barriers embedded in data asset characteristics:

Volatility Imperative: Any debt-for-data arrangement predicated on static baseline carbon intensities faces immediate technical default risk under climate variability or infrastructure disruptions. Carbon accounting infrastructure financing must emphasize real-time monitoring systems rather than periodic reporting based on historical averages. Zambian copper production provides cautionary example. Under normal hydrological conditions, Zambia's copper smelting exhibits extremely low carbon intensity (0.82 tCO₂e per tonne) due to abundant hydroelectric generation from the Zambezi River basin. The 2023-2024 El Niño-driven drought crisis collapsed hydroelectric output, forcing reliance on imported coal power from South Africa's Eskom grid.

Zambia Electricity Supply Corporation documented hydroelectric generation falling 40% below normal capacity during 2023-2024, with deficit met through power imports from the Southern African Power Pool.[75] South Africa's Eskom operates coal-dominant generation fleet with grid emission factor of approximately 0.92 tCO₂/MWh compared to Zambia's normal hydro-based factor of 0.02 tCO₂/MWh. Copper smelting requires approximately 4 MWh per tonne of refined copper. Assuming 40% of smelter electricity demand was met through imported coal power during drought:

Normal: (4 MWh × 0.02 tCO₂/MWh) + 0.74 tCO₂ (process emissions) = 0.82 tCO₂e/tCu

Drought: (2.4 MWh × 0.02) + (1.6 MWh × 0.92) + 0.74 = 2.26 tCO₂e/tCu

This 176% increase demonstrates that any debt-for-data arrangement faces technical default risk under climate variability. The relevant asset becomes the monitoring capability itself rather than any particular carbon intensity claim. Creditors obtain verification capacity; debtors gain infrastructure enabling participation in carbon-constrained trade regimes. But this reframing from "debt relief for demonstrating low carbon intensity" to "debt relief for deploying transparent monitoring infrastructure" shifts value proposition fundamentally. The former proves vulnerable to exogenous factors beyond debtor control. The latter finances tangible physical infrastructure whose value persists regardless of measured outcomes.[76]

Sovereignty Sensitivity: Data sovereignty doctrines operative across Global South create structural barriers absent from nature or infrastructure swaps. India's Digital Personal Data Protection Act (2023) and Indonesia's Government Regulation 71/2019 on data localization directly constrain carbon data flows that debt-for-data arrangements would require. If industrial emissions data becomes classified as "critical data infrastructure" subject to mandatory domestic storage and processing, creditors cannot directly access verification systems, forcing reliance on government intermediaries that undermine the transparency premise.

Thailand's proposed national carbon data sovereignty framework exemplifies these concerns. Industrial process data revealing efficiency levels and technological capabilities constitutes competitive intelligence. Surrendering such data to foreign entities—whether creditors, multilateral institutions, or EU authorities—faces domestic political resistance framed as protecting industrial competitiveness and preventing technological espionage.[77] Unlike marine protected areas where sovereignty assertion enhances rather than conflicts with conservation objectives, carbon data sovereignty directly opposes transparency requirements debt-for-data arrangements demand.

Creditor Asymmetry: Political economy calculus differs substantially between traditional bilateral creditors (Paris Club) and China. Paris Club creditors tend toward rules-based approaches emphasizing financial system stability, with climate additionality as secondary consideration. Climate-resilient debt clauses promoted by France exemplify this: temporary payment suspension during climate disasters without reducing total debt burden, maintaining NPV neutrality while providing short-term relief.[78]

China's approach to debt restructuring emphasizes strategic considerations beyond purely financial returns. The Belt and Road Initiative has generated substantial lending to resource-exporting nations, creating potential alignment between debt relief and supply chain transparency objectives. However, major debt restructurings in Angola and Ethiopia have not included explicit green conditionality, suggesting Chinese preferences for infrastructure-focused arrangements (building physical assets) over policy conditionality.[79] The most promising context for debt-for-data implementation may be the Forum on China-Africa Cooperation framework, particularly regarding critical mineral supply chains where strategic interest in transparent carbon intensity aligns with debt sustainability imperatives.

The asset transmutation framework thus clarifies debt-for-data's conceptual status: theoretically coherent but practically infeasible given current asset characteristics. Data's 4/40 adaptability score reflects not temporary obstacles but fundamental incompatibilities. Nature conservation succeeded because protected areas exhibit spatial boundedness, satellite monitorability, ecological stability, and global public good status. Climate infrastructure achieves moderate success because power plants constitute tangible physical assets despite output volatility. Data fails because it lacks spatial definition, resists objective monitoring, fluctuates radically in value, and triggers acute sovereignty sensitivities. Absent reconceptualization transforming "data" into "monitoring infrastructure"—shifting object from information flows to physical sensor networks—debt-for-data remains speculative rather than operational.

5. Synthesis: Layered Pluralism, Strategic Thresholds, and Implementation Realities

Evidence surveyed across coordination mechanisms and financing innovations reveals an emerging architecture fundamentally different from both universal regulatory convergence and fragmented isolationism. The BASIC coalition's diplomatic coordination, ACMI's market infrastructure, CPA's technical capacity building, and exploratory debt-for-data mechanisms represent complementary rather than competing responses. Together, they sketch outlines of a Global South carbon governance system that could engage with CBAM and similar Northern measures while preserving Southern policy autonomy and developmental priorities.

Several characteristics distinguish this architecture. It embraces institutional multiplicity rather than seeking singular solutions. Rather than establishing one counter-CBAM organization, developing countries cultivate multiple specialized institutions addressing different response dimensions. This polycentricity provides redundancy and flexibility, enabling experimentation and adaptation as circumstances evolve.[80] The architecture prioritizes coordination over convergence. Mechanisms like CPA and ACMI facilitate information exchange and capacity building without requiring members to adopt uniform policies. Countries maintain discretion over domestic carbon pricing levels, sectoral coverage, and revenue utilization while benefiting from shared learning and collective bargaining power.

These mechanisms blend defensive and developmental objectives. While clearly responding to CBAM pressures, initiatives like ACMI simultaneously pursue longstanding goals including mobilizing climate finance for African development and capturing value from natural carbon sinks. Response strategies build enduring institutional capacity rather than merely constructing compliance facades.[81] The architecture leaves strategic ambiguity regarding ultimate confrontation or accommodation with EU standards. By simultaneously pursuing technical capacity building (suggesting eventual compliance) and WTO legal preparation (suggesting potential confrontation), developing countries preserve optionality. This ambiguity may be strategic rather than accidental, maintaining leverage in ongoing negotiations over CBAM implementation details and potential mutual recognition agreements.

Implementation challenges facing these coordination mechanisms should not be underestimated. BASIC's diplomatic unity, while impressive in multilateral forums, masks significant divergences in national circumstances and priorities. China's dual identity as both developing country and world's largest absolute emitter creates tensions within the coalition. South Africa's coal dependence conflicts with other members' renewable energy trajectories. Brazil's agricultural export interests diverge from India's manufacturing focus. The political economy of BASIC coordination reveals deeper structural tensions. China's strategic calculus increasingly emphasizes technological leadership in renewable energy and electric vehicles, creating potential misalignment with India's continued reliance on coal-fired baseload power and South Africa's resistance to rapid coal phase-out that would devastate mining-dependent communities. Brazil's positioning as both agricultural superpower and renewable energy leader creates unique vulnerabilities: agricultural exports face potential CBAM expansion while sugarcane ethanol (RenovaBio credits) seeks recognition as equivalent carbon pricing, forcing simultaneous defensive and offensive strategies.[82]

ACMI's market infrastructure faces scaling challenges extending beyond technical capacity to fundamental questions of credit integrity and additionality. The voluntary carbon market has experienced credibility crises, with investigations revealing many projects claiming emissions reductions would have occurred regardless of carbon finance. African projects must navigate these legitimacy concerns while building institutional capacity for rigorous verification. The tension between ambitious credit generation targets and maintenance of environmental integrity creates potential for either conservative underproduction or aggressive overcrediting, both problematic outcomes.[83]

The governance dynamics within ACMI warrant closer scrutiny. The Regional Voluntary Carbon Markets Company, while nominally an African institution, operates with 80% ownership by Saudi Arabia's Public Investment Fund. This ownership structure raises questions about whose interests the market infrastructure ultimately serves. Gulf states possess strategic motivations for African carbon market development beyond pure climate mitigation: securing carbon offsets to maintain oil production while meeting Paris commitments, establishing financial influence in African economies through carbon credit purchasing power, and potentially using carbon market access as leverage in broader economic relationships. African governments, desperate for climate finance flows, may lack bargaining power to resist terms favorable to Gulf capital.

CPA's technical coordination confronts resource constraints that policy documents often understate. Developing sophisticated MRV systems requires sustained investment in monitoring equipment, data management infrastructure, technical personnel, and quality assurance processes. Many Latin American countries face fiscal constraints limiting such investments, creating dependencies on external technical assistance that may come with conditionalities or methodological preferences aligned with donor rather than recipient priorities.[84]

Toward Policy Experimentation

The framework developed here enables specific experimental designs testable at modest scale. A candidate pilot: Indonesia's nickel sector (€2.1 billion annual EU exports, 15% trade exposure) could negotiate bilateral debt-for-data arrangement with China (holding $4.8 billion Indonesian sovereign debt). Experimental parameters: $200 million debt relief contingent on installing continuous emissions monitoring at 20 largest smelters (representing 65% of export volume) within 18 months. Success metrics: (1) monitoring operational uptime >90%, (2) data integration with EU CBAM registry within 6 months of system activation, (3) reduction in default value penalties by ≥40% for covered installations. If achieved, the model scales; if monitoring uptime <70% or integration fails, infrastructure-first approaches require fundamental redesign. Such experiments would validate or falsify core framework assumptions regarding technical feasibility, creditor incentive alignment, and implementation capacity under real-world constraints.[85]

The strategic ambiguity currently characterizing Global South responses may prove unsustainable as CBAM implementation forces concrete decisions. Countries cannot indefinitely maintain simultaneously that they are building domestic carbon pricing systems demonstrating good faith efforts toward climate action while preparing WTO challenges arguing CBAM violates international trade law. The contradiction between compliance and contestation must eventually resolve into clearer positioning. Some countries will choose accommodation, accepting CBAM framework while negotiating implementation details. Others will choose confrontation, leveraging WTO mechanisms to extract concessions. Still others will pursue hybrid strategies combining selective compliance with diplomatic contestation.

Whether this emerging architecture consolidates into durable institutional arrangements or fragments under implementation pressures depends on developments beyond analytical prediction: the EU's willingness to accommodate alternative methodologies through mutual recognition agreements, China's strategic choices in FOCAC negotiations balancing debt sustainability with supply chain transparency imperatives, and the resilience of BASIC coordination under distributional pressures as abstract principles confront concrete trade-offs. By 2027-2028, when CBAM certificate purchases create actual financial flows and WTO disputes potentially reach panel stages, the architecture's durability will face definitive tests.

6. Conclusion

January 2026 marks an inflection point. CBAM's transitional reporting phase has concluded, certificate purchases loom for 2027, and the EU's Omnibus amendments have clarified compliance requirements. Developing countries have moved beyond initial confusion toward systematic response. The coordination mechanisms documented here—BASIC's UN procedure weaponization, ACMI's market infrastructure, CPA's technical alignment, exploratory debt-for-data frameworks—collectively constitute a nascent architecture enabling selective engagement with carbon-constrained trade while preserving policy autonomy.

This architecture will not produce universal regulatory convergence. Preliminary analysis suggests non-linear relationships between trade exposure and strategic response: countries with extreme exposure (>40%) pursue comprehensive alignment; those with moderate exposure and institutional capacity (15-30%) construct defensive interoperability systems; nations with minimal exposure leverage diplomatic coordination without domestic policy restructuring. The predicted 25% exposure threshold suggests a critical transition point where strategic postures shift from diplomatic positioning to operational compliance adaptation. The resulting landscape proves more complex than either harmonization optimists or fragmentation pessimists anticipate.

Systematic evaluation of Ostrom's polycentric governance principles reveals why observed coordination operates in defensive rather than cooperative mode. Structural failures in collective choice (BASIC excluded from EU rule-making), monitoring reciprocity (unidirectional EU oversight), and nested enterprise (CBAM bypassing UNFCCC) transform coordination from mutual adjustment among equals into organized resistance against monocentric imposition. The theoretical implication extends beyond CBAM: polycentric governance under extreme power asymmetry becomes governance against hierarchy rather than governance through deliberation.

Asset transmutation theory explains variance in debt-for-X success rates. Nature assets' 36/40 adaptability score (spatial definability, monitorability, volatility stability, low sovereignty sensitivity) produces 83% success rate across six major transactions. Infrastructure assets' 23/40 score suggests moderate feasibility pending verification through larger sample. Data assets' 4/40 score indicates structural barriers: absent reconceptualization shifting object from information flows to physical monitoring infrastructure, debt-for-data remains conceptual rather than operational.

For policymakers in developing countries, effective CBAM response requires moving beyond purely national strategies toward active participation in coordination mechanisms. The counterfactual analysis—τ increasing from 0.18 to 0.35 absent coordination, representing €15 billion annually—quantifies coordination's economic value. This magnitude exceeds total climate adaptation finance flows to the Global South, placing coordination mechanisms' material significance in stark relief rather than treating them as merely symbolic political gestures.

For European policymakers, the emerging coordination signals that CBAM will not produce simple convergence. Expecting uniform global adoption of EU frameworks ignores institutional diversity and path dependencies characterizing national climate governance systems. More realistic outcomes involve proliferation of mutual recognition agreements, acceptance of alternative methodologies demonstrating equivalence, and iterative adjustment of CBAM rules to accommodate legitimate concerns. The digital sovereignty complications—data localization laws potentially increasing compliance costs 12-18%—exemplify unintended interactions between regulatory domains that EU policymakers must navigate.

The transition from climate cooperation to carbon trade confrontation represents a fundamental shift in international environmental governance. Where previous decades emphasized voluntary commitments and multilateral coordination through UN processes, the CBAM era links environmental standards directly to market access. This transformation creates both risks of trade fragmentation and opportunities for institutional innovation. Which trajectory prevails will be determined substantially by how effectively developing countries convert defensive responses into durable coordination architectures capable of shaping rather than simply reacting to Northern regulatory initiatives.

The framework generates falsifiable predictions enabling empirical validation as CBAM implementation proceeds. If Indonesia's nickel sector pilot proceeds as outlined—$200 million debt relief for 20-smelter monitoring coverage—results observable by late 2027 would validate or falsify predictions regarding infrastructure costs, operational feasibility, and creditor incentive alignment. Similarly, if Brazil's trade exposure crosses the predicted 25% threshold without triggering strategic repositioning, the threshold effect hypothesis requires revision. If BASIC coordination intensifies at moderate rather than high exposure levels, the inverted-U hypothesis gains support.

The evidence suggests coordination architectures are emerging, albeit incompletely. Their ultimate significance depends on future developments beyond current visibility. What seems increasingly certain is that CBAM catalyzes institutional innovation as developing countries construct governance architectures enabling engagement with carbon-constrained trade regimes while preserving autonomy over core policy choices. The result may be a more pluralistic and complex global carbon governance system than either universal harmonization optimists or fragmentation pessimists anticipate. This complexity, while creating coordination challenges, may better accommodate the enormous diversity in national circumstances, capabilities, and developmental priorities characterizing the contemporary international system.

References

[1] European Commission. (2023). Regulation (EU) 2023/956 establishing a Carbon Border Adjustment Mechanism. Official Journal of the European Union, L 130.

[2] UN Comtrade Database. (2024). Trade statistics by commodity and partner country. Geneva: United Nations.

[3] United Nations Framework Convention on Climate Change. (2015). Paris Agreement. Article 2(2) and Article 4(3).

[4] Global Carbon Project. (2024). Supplemental data of Global Carbon Budget 2024. https://doi.org/10.18160/gcp-2024

[5] Mehling, M. A., et al. (2019). Designing border carbon adjustments for enhanced climate action. American Journal of International Law, 113(3), 433-481.

[6] Van Asselt, H., & Mehling, M. (2021). The Role for WTO Law in Addressing Climate Change. Geneva: World Trade Organization.

[7] Jordan, A., Huitema, D., Van Asselt, H., & Forster, J. (2018). Governing Climate Change: Polycentricity in Action? Cambridge University Press.

[8] Republic of Turkey Ministry of Environment, Urbanization and Climate Change. (2024). Turkish ETS Design Consultation Document. Ankara.

[9] Ministry of Environment, Forest and Climate Change, Government of India. (2023). India's Updated Nationally Determined Contribution. New Delhi.