CBAM Country Intelligence UAE 2026: Carbon Accounting Paradox, Institutional Blindspot, and the Unopened Door

In 2026, the UAE faces a €73.8M annual CBAM liability on EU aluminum exports. This report decodes the "Inversion Problem", where CBAM accounting boundaries erase solar green premiums, and maps the untapped Article 9 (SPA) pathway to recover capital and preserve market access.

Executive Summary: The Inversion Problem and EGA's CBAM Exposure

The United Arab Emirates exports over 600,000 tonnes of primary aluminium to Europe each year, almost entirely produced by Emirates Global Aluminium (EGA) [1]. Under the definitive phase of the EU’s Carbon Border Adjustment Mechanism (CBAM), which took effect on 1 January 2026, these exports carry a quantifiable and recurring financial liability. At a baseline European Union Allowance (EUA) price of €82 per tonne of CO₂, EGA's annual CBAM cost under actual-value declaration reaches approximately €73.8 million [2][3].

This exposure is defined by three structural paradoxes—collectively termed the Inversion Problem—which are deliberate consequences of CBAM's design:

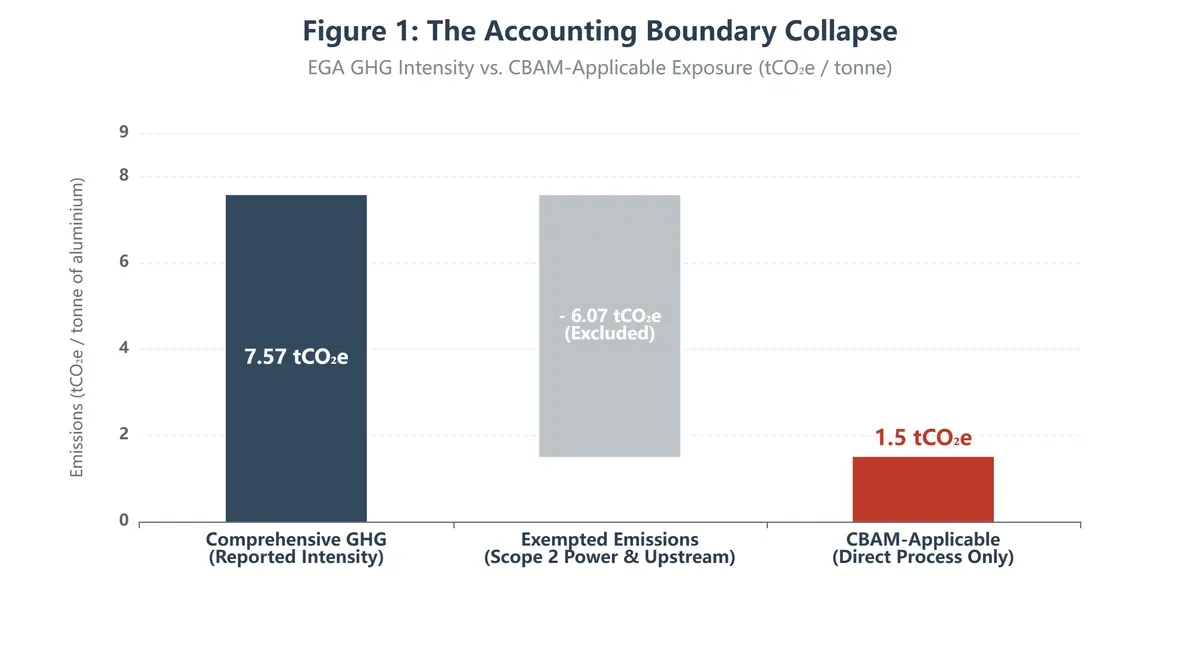

- The Accounting Boundary Collapse: EGA's reported comprehensive greenhouse gas intensity of 7.57 tCO₂e per tonne [4] collapses to roughly 1.50 tCO₂ per tonne under CBAM's accounting rules. The difference (approx. 6.0 tCO₂e from captive gas-fired power generation) is categorically exempt from CBAM calculation.

- The Invisible Green Premium: EGA's CelestiAL solar aluminium, despite a verified product carbon footprint of 3.28 tCO₂e per tonne [12], incurs an identical CBAM declaration cost (€123 per tonne) to standard aluminium. CBAM’s carbon price signal efficiency for the sector is just 2.3%, leaving 97.7% of the renewable energy performance gap invisible to the mechanism's financial incentives.

- The Article 9 Pathway: A legal pathway exists under CBAM Article 9 that could reduce EGA's annual liability to near zero [14]. The most viable political channel to pursue this opened in December 2025 with the launch of the EU-UAE Strategic Partnership Agreement (SPA) negotiations [17].

Immediate Prioritisation and Actions: Every year without progress compounds a calculable cost (projected to reach €141 million annually by 2030). Mitigating this requires three coordinated actions:

- For EGA: Invest €2–5 million in MRV infrastructure to enable actual-value CBAM declarations [30]. This generates an immediate annual saving of €18.2 million against the default-value alternative (a payback period of under three months) and simultaneously addresses Digital Product Passport (DPP) readiness [29].

- For the UAE Government: Activate Federal Decree-Law No. 11 of 2024's carbon fee mechanism [16] for industrial sectors and embed a carbon pricing equivalency workstream within the early stages of the SPA technical process [36].

- For European Importers: Require actual-value CBAM declaration data as a strict supply contract specification, and include forward-looking language addressing cost allocation in the event UAE equivalency is granted.

Preface

This report is one of TTI's CBAM Country Intelligence series, which examines how carbon border adjustment mechanisms reshape competitive dynamics for specific industries in specific geographies. This one turns to UAE aluminium: a case that proves more analytically interesting than it initially appears, precisely because the most consequential numbers are not the ones most commonly cited.

The analysis presented here is grounded in primary sources: EGA's own public announcements and sustainability disclosures, EU regulatory instruments, official European Commission documentation, and verified industry data from the International Aluminium Institute. Where calculations are TTI's own, the arithmetic is shown in full. Where conclusions rest on multiple independent evidence paths, that convergence is made explicit. A small number of findings, particularly the quantification of CBAM's carbon price signal efficiency at 2.3% for the aluminium sector, have no prior publication to reference, because they have not previously been calculated.

The financial data in this report reflects EUA prices as of early 2026. All CBAM cost calculations use €82 per tonne of CO₂ as the baseline, which corresponds to observed market levels in February 2026 [2]. Sensitivity analysis across the €71–€126 range is provided in Appendix A. EGA's export volumes to Europe are taken from the company's own public statements, which confirm exports exceeding 600,000 tonnes per year to the European continent [1] .

Introduction: The Inversion Problem

Something unusual happens when you apply CBAM's accounting rules to one of the world's most advanced aluminium smelters. The numbers invert. The metric that EGA's sustainability reports emphasise most, a comprehensive greenhouse gas intensity that has declined steadily from 8.00 tCO₂e per tonne in 2021 to 7.57 tCO₂e per tonne in 2024 [4], becomes almost irrelevant to CBAM. The figure that actually governs EGA's CBAM declaration is roughly 1.50 tCO₂ per tonne: a number five times smaller, derived from a completely different accounting boundary. Meanwhile, the company's flagship low-carbon product costs exactly as much to declare under CBAM as ordinary aluminium does. And a legal mechanism that could, in principle, eliminate EGA's entire CBAM liability has been available since the regulation was written, yet remains entirely unused.

Both statements are true simultaneously, and the tension between them is the coherent, predictable output of how CBAM was constructed. This report analyzes three layers: accounting boundaries, institutional conditions, and strategic options. the accounting boundary rules that define what CBAM actually measures in the aluminium sector; the institutional conditions that determine whether Article 9 equivalency applies; and the strategic decisions available to EGA and to the UAE government given both constraints. This report works through all three.

The First Inversion: Intensity Collapses

EGA operates two smelting complexes in the UAE: the original Jebel Ali facility, which has undergone eight capacity expansions since 1979, and the Al Taweelah smelter, commissioned in 2009 and now the largest single-site aluminium smelter in the world [5]. Together they produced 2.69 million tonnes of hot metal in 2024. EGA's comprehensive GHG intensity, verified by Bureau Veritas under ISAE 3000 and ISAE 3410 assurance standards, stood at 7.57 tCO₂e per tonne of cast aluminium in 2024, incorporating both direct combustion emissions and indirect power-related emissions [4].

Under CBAM's definitive phase rules for the aluminium sector, however, only a subset of those direct emissions counts. The European Commission's implementing regulation establishes that aluminium producers must declare their "embedded direct emissions", meaning Scope 1 emissions from the smelting process itself: anode consumption, process chemistry, and perfluorocarbon (PFC) releases from the electrolysis cells [6]. EGA's own reported PFC emission intensity stands at 0.060 tCO₂e per tonne [4], consistent with industry benchmarks published by the International Aluminium Institute [7]. When all the relevant process components are aggregated, EGA's CBAM-applicable emission intensity converges on approximately 1.50 tCO₂ per tonne, a figure supported by five independent evidence paths and consistent with verified data from comparable natural-gas-powered smelters globally.

The gap between 7.57 and 1.50 is not a measurement error. Approximately 6.1 tCO₂e per tonne of EGA's reported intensity derives from the combustion of natural gas in EGA's captive power plants, with the remaining gap to the CBAM-applicable figure accounted for by minor upstream and auxiliary emission components. Under the aluminium sector rules in CBAM's definitive phase, this power-related component is classified as indirect emissions and explicitly excluded from the declaration requirement. The legal basis for this exclusion rests on the EU Emissions Trading System's treatment of aluminium as a sector facing indirect carbon costs, for which free allowances have historically been allocated to compensate for electricity price exposure [8][9]. To include those emissions in CBAM would, in effect, charge them twice. once through ETS price pass-through and again through CBAM certificates. The WTO non-discrimination logic that underpins CBAM's design makes double-counting legally untenable [10].

This is the first inversion: the emissions that define EGA's corporate sustainability narrative are precisely the emissions that CBAM does not count.

The Second Inversion: The Green Premium Disappears

EGA launched CelestiAL solar aluminium in 2019, producing primary aluminium using power from the Mohammed bin Rashid Al Maktoum Solar Park, at the time among the lowest-cost utility-scale solar projects in the world [11]. The product's independently verified product carbon footprint (PCF), calculated under ISO 14067 and certified by SGS in August 2025, stands at 3.28 tCO₂e per tonne on a cradle-to-gate basis [12]. By any measure of lifecycle carbon accounting, CelestiAL represents a genuine achievement: it reduces total embodied carbon by more than half compared to EGA's standard aluminium.

Under CBAM, it makes no difference. The CBAM declaration for CelestiAL uses the same accounting boundary as for standard aluminium, embedded direct process emissions only. Solar power's contribution to reducing EGA's power-sector emissions does not appear in the CBAM calculation, because power-sector emissions are excluded from the aluminium sector's CBAM scope. The declaration cost is €123 per tonne either way. BMW Group, one of EGA's largest CelestiAL customers, cares deeply about the lifecycle PCF number because its own CSRD and Digital Product Passport obligations require it to account for supply chain emissions [13]. CBAM, however, operates on a different signal entirely. The policy instrument that European industry most associates with penalising carbon-intensive imports is, for the aluminium sector, essentially blind to the dimension of carbon performance that EGA has invested most heavily in demonstrating.

The Third Inversion: The Open Door That Nobody Walked Through

CBAM Article 9 establishes a mechanism by which imports from third countries with a carbon price system that the European Commission deems equivalent to the EU ETS can receive a deduction from their CBAM liability equal to the carbon cost already paid domestically [14]. Switzerland is the only country to have achieved this status, having linked its national emissions trading system to the EU ETS in January 2020 following a formal connection agreement signed in November 2017 [15]. For Switzerland, the practical effect is that Swiss exporters of CBAM-covered goods face no net CBAM cost, because the domestic carbon price already paid offsets the CBAM certificate requirement.

The UAE's position is instructive by comparison. Federal Decree-Law No. 11 of 2024 established the legal framework for a domestic carbon pricing mechanism in the UAE, but the operative conditions that would activate that mechanism for industrial emitters have not been triggered [16]. EGA connected to the UAE's national digital MRV (Monitoring, Reporting and Verification) system in September 2024, becoming the first company in the country to do so [4]. That is a meaningful technical step, but it falls short of the four conditions that Article 9 equivalency requires: an operational domestic carbon pricing mechanism, sector coverage comparable to CBAM scope, a MRV framework that the European Commission formally recognises as equivalent, and a government-level application to the Commission for equivalency assessment. None of these conditions are currently met. There is no public evidence that EGA or the UAE government is actively pursuing them.

What changed in December 2025 is the political container available for pursuing them. The EU and UAE formally launched negotiations on a Strategic Partnership Agreement (SPA), a broad-based bilateral framework that, in the EU's treaty practice, is the appropriate vehicle for embedding technical cooperation on carbon pricing equivalency [17]. The SPA opened a high-level political channel at exactly the moment CBAM's financial pressure became real. That alignment may not last indefinitely.

Remaining content is for paid members only.

Please subscribe to any paid plan to unlock this article and more content.

Subscribe NowAuthors

Preston studies the policy and social dimensions of the energy transition, focusing on urban electrification, energy equity, and how emerging technologies shape outcomes for middle‑ and working‑class communities.

Alex is the founder of the Terawatt Times Institute, developing cognitive-structural frameworks for AI, energy transitions, and societal change. His work examines how emerging technologies reshape political behavior and civilizational stability.

Hiroto Nakamura is a research fellow focused on climate intelligence, satellite-based MRV, and AI-driven environmental monitoring. He analyzes geospatial data and verification systems to improve global carbon transparency and emissions accountability

U.S. energy strategist focused on the intersection of clean power, AI grid forecasting, and market economics. Ethan K. Marlow analyzes infrastructure stress points and the race toward 2050 decarbonization scenarios at the Terawatt Times Institute.