Abstract

As the European Union's Carbon Border Adjustment Mechanism (CBAM) imposes compliance obligations on carbon-intensive imports, developing economies confront a structural accounting gap: their industries have already paid substantial implicit carbon costs through fuel taxes and regulatory compliance, yet these expenditures remain unrecognized in international carbon pricing frameworks. This article introduces Digital Cost Certificates (DCC), a blockchain-based mechanism that transforms historically paid policy costs into verifiable credentials within a standardized accounting interface.

DCC does not create new carbon credits or undermine CBAM's environmental integrity. Rather, it provides a technical layer for recognizing previously incurred policy costs within existing compliance frameworks, subject to bilateral or multilateral recognition agreements. Unlike the failed Clean Development Mechanism, which collapsed under the burden of proving counterfactual additionality, DCC validates factual payment records through tax authority database integration. Through theoretical modeling and empirical case studies spanning India's steel sector and China's national emissions trading system, we demonstrate that verified implicit carbon pricing recognition could adjust effective CBAM exposure by 15-35% under negotiated recognition coefficients, while maintaining environmental integrity through conservative α calibration and robust anti-gaming mechanisms.

We propose a three-tiered conceptual trading architecture combining concentrated liquidity automated market makers for retail participation with request-for-quote systems for industrial-scale transactions. Recognition coefficient α, governing the extent of implicit carbon price acknowledgment in CBAM calculations, emerges as a dynamic equilibrium shaped by verification costs, penalty structures, and information asymmetry. Our roadmap projects α evolution from 0.25 in bilateral pilot phases (2026-2027) to 0.50-0.70 under multilateral frameworks by 2030, contingent on demonstrated data integrity and compliance with international trade law. The framework offers developing nations an accounting mechanism for climate policy costs already incurred, converting compliance burden into documented contributions toward decarbonization objectives.

1. Introduction: The Accounting Gap

India's Finance Minister confronts a fiscal paradox. The country's fuel excise duties embed an implicit carbon price of approximately ₹1,993 per ton of CO₂ through diesel consumption taxes, translating to roughly €22 per ton at current exchange rates [1]. Across energy-intensive export sectors, this generates an annual implicit carbon expenditure exceeding €2.1 billion. Yet under CBAM's implementing regulations, these costs vanish from compliance accounting. The regulation recognizes only explicit carbon pricing through emissions trading systems or direct carbon taxes meeting specific methodological criteria detailed in Annex IV [2]. India's fiscal contributions, instrumentalized through fuel taxation to discourage carbon-intensive consumption, receive no acknowledgment in CBAM liability calculations. The result resembles double taxation: domestic policy costs first, border adjustment obligations second.

Traditional economic analysis frames this as irrecoverable sunk cost. The DCC framework challenges this assumption by reconceptualizing implicit carbon expenditures as verifiable contributions toward climate objectives. Every rupee paid in fuel excise, every yuan locked in mandatory energy efficiency certificates, represents not merely fiscal burden but documented evidence of policy-driven decarbonization costs. These payments constitute verifiable historical facts, recorded through tax receipts and regulatory filings, fundamentally different from the prospective reduction claims that plagued voluntary carbon markets. Where carbon credits promise future emission cuts requiring complex baseline construction, DCC simply certifies past payments. This distinction matters profoundly for verification architecture and trust dynamics.

The conceptual shift from compliance burden to accounting asset follows established patterns in financial infrastructure evolution. Mortgage-backed securities transformed illiquid housing loans into tradable instruments by creating standardized documentation. Carbon markets attempted similar transformation with emission rights. DCC extends this logic to policy costs themselves, recognizing that regulatory compliance generates quantifiable value beyond legal obligation fulfillment. An Indian steel mill paying ₹16.84 crore annually in mining diesel taxes [3] has made verifiable contributions toward carbon price signals that influence fuel consumption decisions. The question becomes whether international frameworks can acknowledge these contributions through systematic accounting mechanisms, creating recognition pathways while maintaining environmental integrity safeguards.

This research does not propose replacing or circumventing CBAM. Rather, it develops a complementary accounting interface that could operate within CBAM's existing structure, subject to negotiated recognition parameters. The DCC mechanism addresses a specific technical gap: the absence of standardized protocols for verifying and crediting implicit carbon costs in border adjustment calculations. By providing this interface layer, the framework enables policy dialogue around recognition criteria, verification standards, and appropriate discount factors, transforming what is currently an accounting void into a structured negotiation space.

2. First Principles: Why DCC Succeeds Where CDM Failed

The Clean Development Mechanism's collapse offers instructive lessons in carbon market design. Between 2011 and 2012, Certified Emission Reduction (CER) prices plummeted from €7 to €0.81 per ton, an 88% decline driven by fundamental architectural flaws [4]. The mechanism required project proponents to demonstrate additionality through counterfactual reasoning: proving that emission reductions would not have occurred absent CDM incentives. This epistemological burden proved insurmountable at operational scale. With over 230 approved methodologies fragmenting the verification landscape [5], the system became simultaneously too complex for efficient administration and too porous for credible assurance. Baseline construction debates consumed years, allowing project sponsors to game assumptions while genuine innovators faced prohibitive transaction costs.

Voluntary carbon markets inherited these pathologies with predictable results. Recent investigations revealed that over 90% of Verra-certified rainforest projects failed to deliver claimed protection benefits [6]. The Guardian's analysis, cross-referencing satellite imagery with project boundaries, demonstrated systematic overestimation of deforestation baselines. Projects claimed credit for preventing forest loss that was never credibly threatened. The 2023 market contraction, with trading volumes declining 61% from peak levels [7], reflected fundamental loss of buyer confidence. The pattern repeats: construct verification frameworks based on unobservable counterfactuals, observe systematic gaming as market pressures incentivize optimistic assumptions, watch market credibility collapse under investigative scrutiny.

DCC architecture avoids this trap through evidentiary simplicity rooted in verifiable historical facts. Consider India's fuel taxation structure, documented through parliamentary records and Ministry of Petroleum publications. Central excise duties on diesel stand at ₹15.80 per liter, while state value-added taxes add approximately ₹13.44 per liter in major industrial states like Odisha and Jharkhand [8]. These rates apply uniformly to commercial diesel purchases, creating an implicit carbon cost unavoidable for energy-intensive industries. A steel producer consuming 57.6 million liters annually for mining operations and internal logistics faces combined tax liabilities of ₹168.42 crore (approximately €18.3 million). These figures appear on audited financial statements, cross-verified through Goods and Services Tax Network databases and state commercial tax departments [9].

The verification logic shifts from proving "what would have happened" to confirming "what actually happened." This transforms DCC issuance into a database reconciliation problem rather than a causal inference challenge. When an enterprise submits a DCC generation request, the validation engine performs three checks. First, does the submitted tax receipt exist in government revenue records? Second, has this specific payment already generated a DCC, preventing double-counting? Third, does the conversion ratio comply with established formulas? Affirmative answers trigger DCC credential issuance. The entire process can execute algorithmically through API integration with national tax systems, eliminating the methodological approval bottlenecks that plagued CDM's project-by-project reviews.

Why haven't alternative solutions to the CBAM recognition gap gained traction? Modifying CBAM regulations faces political improbability. The mechanism emerged from decade-long negotiation, hardened through multiple European Parliament readings and Council compromise packages [10]. Any substantive amendment requires repeating this legislative gauntlet with uncertain outcomes. Establishing parallel carbon markets invites the same verification failures that destroyed CDM credibility, while potentially creating competing standards that fragment rather than integrate global carbon pricing. WTO litigation offers theoretical recourse but practical futility. Even successful dispute resolution extends 7-10 years while competitive damage accumulates [11]. Meanwhile, trade relations suffer broader deterioration as climate policy becomes weaponized in geopolitical competition.

DCC circumvents these obstacles by working within existing legal frameworks rather than demanding their modification. It accepts CBAM's fundamental structure as given while creating an auxiliary accounting layer for implicit carbon price recognition. The mechanism does not require EU legislative action for initial deployment. Bilateral recognition agreements can establish pilot frameworks through administrative procedures, similar to mutual recognition arrangements in customs cooperation or regulatory equivalence determinations in financial services. This modular approach enables experimentation and learning without committing to permanent institutional changes, reducing political resistance and facilitating adaptive refinement based on operational experience.

3. Technical Standard: The DCC Architecture

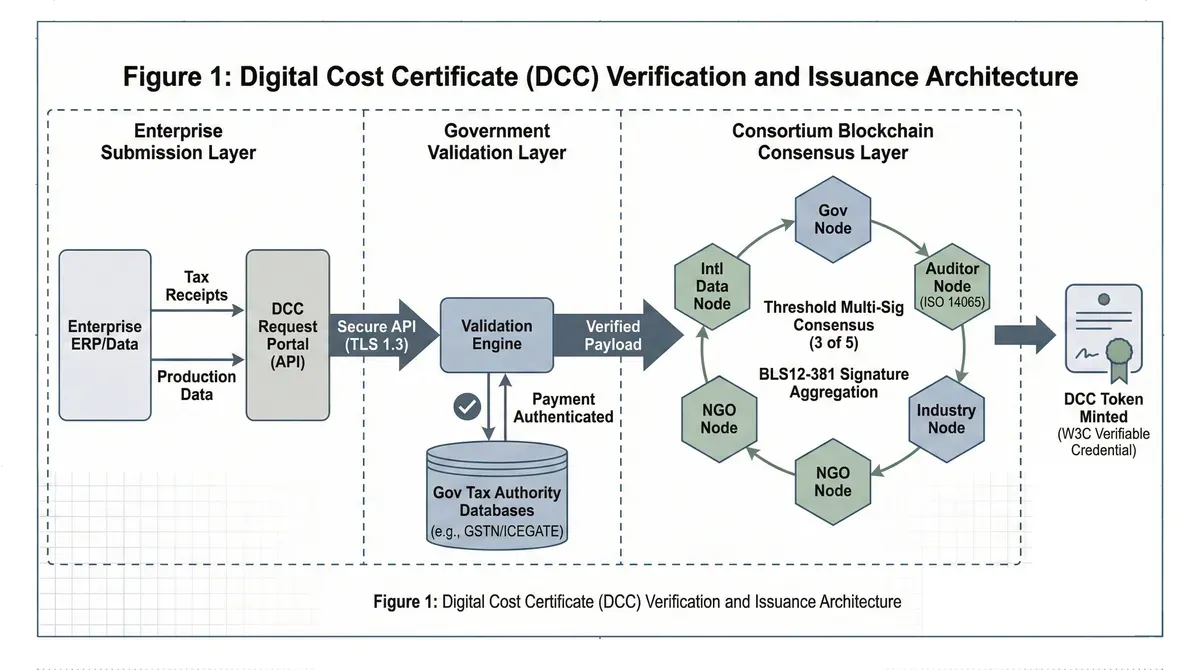

At its technical core, a Digital Cost Certificate functions as a W3C Verifiable Credential, containing cryptographically signed attestations about policy cost payment [12]. Each DCC encodes several data elements structured for interoperability and verification. The credential header specifies the issuing entity, typically a government agency with tax administration authority or delegated verification powers, along with issuance timestamp using ISO 8601 format and expiry date tied to fiscal reporting cycles. The payload contains the quantified carbon cost expressed in standardized units (€/tCO₂ equivalent), the specific policy instrument generating the cost (fuel excise duty, emissions trading allowance purchase, renewable energy certificate procurement), and the precise time period covered with start and end dates.

The underlying policy instrument classification matters significantly for recognition eligibility. Fuel excise duties on commercial diesel or industrial coal consumption create direct, measurable costs per unit of carbon content, facilitating straightforward conversion formulas. For instance, India's combined central and state diesel taxes of ₹29.24 per liter [8], when divided by diesel's emission factor of 2.68 kgCO₂ per liter [13], yield an implicit carbon price of ₹10.91 per kgCO₂, or approximately €1,184 per ton at ₹92/€ exchange rates. Emissions trading system allowance purchases similarly generate verifiable costs through auction records or secondary market transactions. However, renewable energy subsidies or energy efficiency standards create more complex valuation challenges, potentially requiring policy-specific methodologies and tiered recognition under different α coefficients.

Unlike carbon credits measuring prospective emission reductions, DCC quantifies retrospective expenditures. A credential bearing the designation "1 DCC Unit = €22 implicit carbon cost" certifies that the holder previously paid €22 in fuel taxes containing carbon pricing elements, not that they reduced emissions by one ton relative to a hypothetical baseline. This distinction proves crucial for verification architecture. Carbon credit validation demands continuous emission monitoring systems, baseline calculations requiring sectoral benchmarks and historical trend analysis, and counterfactual modeling to demonstrate additionality. DCC validation requires only tax receipt authentication and payment confirmation through government revenue systems, essentially solved problems in modern digital fiscal administration.

The generation workflow begins with enterprise data aggregation and submission. Using India's proposed Green Export License framework as template [14], firms compile audited annual reports to the Directorate General of Foreign Trade detailing fuel consumption by source type (diesel for mining equipment, coal for process heat, natural gas for ammonia synthesis), associated tax payments with transaction identifiers, and production output for intensity calculations. The conversion formula operates through transparent arithmetic: each ₹100,000 in non-refundable implicit fuel taxes generates one DCC unit at standardized valuation. For Tata Steel's FY2023-24 operations, with 57.6 million liters of diesel consumption bearing ₹29.24 per liter combined tax burden, total eligible expenditure reaches ₹1,684,224,000, yielding 16,842 DCC units under this conversion ratio [3].

Government validation systems cross-reference submitted claims against tax authority databases through secure API connections. The process mirrors existing mechanisms like India's RoDTEP scheme, which already validates indirect tax payments for export duty remission purposes through ICEGATE customs automation infrastructure [15]. Indian steel exporters submit consumption data alongside GST registration numbers and assessment year identifiers. The validation engine queries both central excise records maintained by the Central Board of Indirect Taxes and Excise and state commercial tax databases through the GST Network's unified platform. Response data confirms payment authenticity, matches declared amounts, and flags any discrepancies for manual review.

Once verified, the system mints DCC tokens on a consortium blockchain governed through multi-signature validation requiring consensus among designated verification nodes. This distributed architecture prevents unilateral manipulation. A five-node configuration might include government regulatory representatives, accredited third-party auditors certified under ISO 14065 verification standards, industry association technical committees providing sector expertise, environmental NGOs ensuring civil society oversight, and international data exchange platforms maintaining cross-border interoperability. Credential issuance requires threshold signatures from at least three nodes, ensuring that no single entity controls creation while maintaining processing efficiency through partial decentralization.

The blockchain substrate employs BLS12-381 signature aggregation, allowing multiple validators to combine attestations into a single cryptographic proof [16]. When five verification nodes each independently validate a submission against their respective criteria, their individual signatures aggregate mathematically into one composite proof. On-chain verification requires checking this aggregated signature against the combined public key, a constant-time operation regardless of validator count. This architecture preserves decentralization benefits while avoiding Ethereum mainnet's transaction fee burden, which would render micropayment-scale DCC generation economically prohibitive. A consortium chain using Proof of Authority consensus with known, accountable validators provides the appropriate balance between security, efficiency, and regulatory oversight for government-backed credentials.

4. Three Use Cases and CBAM Integration

4.1 Internal Offset: Monetizing Regulatory Efficiency

The Internal Offset Mechanism (IOM) represents DCC's most distinctive application, transforming regulatory compliance costs into tradable velocity through administrative process optimization. Traditional subsidy mechanisms drain fiscal resources through direct cash transfers or tax expenditures. IOM creates value at near-zero marginal government cost by exchanging DCC credentials for non-monetary export facilitation, specifically manifest as customs processing acceleration, regulatory inspection exemptions, and production quota priority allocations. This architectural choice addresses a fundamental constraint in developing economy climate policy: limited fiscal space for green subsidies amid competing development priorities.

India's Green Export License design provides operational specificity for this conceptual framework. Under the 2023 Foreign Trade Policy, the government explicitly shifted from "incentive-based" to "remission-based" export support to ensure WTO compliance and reduce anti-dumping vulnerability [17]. However, steel products classified under Harmonized System Chapter 72 face systematic exclusion from major benefit schemes like the Remission of Duties and Taxes on Exported Products (RoDTEP) due to fiscal budget constraints and international anti-subsidy investigation risks [18]. This creates a policy vacuum where industries facing the most severe CBAM pressure receive the least domestic support for transition investments.

The GEL framework addresses this gap by offering regulatory velocity rather than fiscal transfers. Enterprises holding verified DCC credentials gain Direct Port Entry (DPE) status, bypassing Container Freight Station intermediate handling and routing factory-sealed containers directly to terminal berths [19]. This privilege compresses cargo dwell time from seven days under standard CFS processing to approximately two days under DPE fast-track protocols [20]. Additionally, GEL holders access zero-inspection lanes available to Authorized Economic Operator Tier-3 certified entities, ensuring export release order issuance within 24 hours except under specific intelligence alerts flagging high-risk shipments [21]. Port fee waivers and priority berthing allocation during congestion periods provide further operational advantages.

The fiscal closed-loop operates through asymmetric value creation where government revenue remains intact while enterprise efficiency improves. Unlike RoDTEP cash refunds, which would cost the treasury ₹10 crore annually for a firm exporting ₹1,000 crore of steel at hypothetical 1% remission rates, GEL requires only marginal administrative expenses. The ICEGATE customs automation system needs minimal software modification to flag DCC-holding accounts in shipment risk profiling algorithms [22]. Port infrastructure bears no additional capital burden, as faster cargo throughput actually improves existing asset utilization ratios. Terminal operators process more containers per berth-day, increasing revenue productivity without capacity expansion. Against these negligible incremental costs, the government retains full fuel tax revenue streams. Tata Steel's ₹168.42 crore annual diesel tax payments remain in national coffers, financing public infrastructure and social programs while the enterprise gains velocity benefits [3].

Enterprise returns decompose into three quantifiable components with different realization mechanisms. Direct logistics cost savings emerge from eliminated CFS handling charges, conservatively estimated at ₹8,000 per twenty-foot equivalent unit (TEU) based on Jawaharlal Nehru Port Trust operational benchmarking [23]. For Tata Steel's approximately 50,000 TEU annual export volume, assuming 50% containerization of 2.5 million tons total exports at 25 tons per container average weight, this yields ₹40 crore in operational cost reduction flowing directly to bottom-line profitability. These savings accrue immediately upon DPE implementation without requiring working capital investment or process redesign.

Working capital interest savings follow from reduced cargo dwell time and accelerated cash conversion cycles. Each containerized steel shipment represents approximately ₹13.75 lakh in inventory value, calculated using current hot-rolled coil prices around ₹55,000 per ton [24] multiplied by 25-ton container payload. Five-day dwell time reduction releases this capital for productive deployment or debt service reduction. At Tata Steel's weighted average cost of capital of 10.64% annually [25], each day saved generates ₹400 in opportunity cost recovery per TEU. Across 50,000 containers, five-day acceleration produces ₹10 crore annual benefit in reduced financing costs or improved cash flow management. For capital-intensive industries operating on thin EBITDA margins, this working capital velocity enhancement carries strategic value beyond nominal interest calculations.

Demurrage avoidance constitutes the third benefit category, estimated conservatively at ₹2.5 crore annually assuming 5% shipment contingency rates encountering delays requiring penalty fees averaging ₹10,000 per incident. Port congestion, customs documentation discrepancies, or inspection triggers can strand cargo beyond free time periods, triggering exponential demurrage charges that rapidly exceed shipment value. GEL's zero-inspection priority and guaranteed 24-hour processing eliminate these tail risks, providing insurance value that conventional cost accounting understates.

The cumulative ₹52.5 crore annual benefit represents 31.2% recovery of sunk fuel tax costs. While this incomplete coverage might appear insufficient at first analysis, such assessment misses the mechanism's fundamental economics. Without GEL, the ₹168.42 crore tax burden remains permanently stranded as pure cost with zero offsetting benefit. With GEL implementation, ₹52.5 crore gets monetized through velocity conversion, transforming dead weight into productive value. For steel industry operators confronting single-digit EBITDA margins and intense import competition, this 31% recovery constitutes transformative competitive advantage. The comparison benchmark is not hypothetical full tax refund, which faces insurmountable fiscal and WTO constraints, but rather current zero-recovery baseline against which any positive return generates real value.

China's approach targets carbon allowance allocation mechanisms rather than customs processing infrastructure, reflecting its distinct institutional architecture centered on national emissions trading systems. The 2024-2025 National ETS allocation plan for steel, cement, and aluminum sectors employs intensity-based formulas with performance adjustments capped at ±3% from baseline benchmarks [26]. The methodology calculates: Allowance Volume ≈ Actual Production Output × Sector Benchmark Emission Intensity × (1 ± Performance Adjustment Factor). Enterprises demonstrating superior emission intensity through verified process improvements receive up to 3% additional free allowances above baseline allocation requirements, while poor performers face proportional reductions creating compliance deficits.

DCC integration occurs through three distinct but complementary pathways, each targeting different temporal and verification dimensions. First, enterprises submit DCC credentials derived from verified low-carbon technology investments or contracted green electricity procurement to receive virtual emission intensity adjustments in baseline calculations. These credits modify the denominator in intensity formulas, effectively lowering calculated emissions per unit output. A steel mill documenting ₹50 crore investment in waste heat recovery systems generating DCC at prescribed conversion ratios could adjust its baseline intensity from 2.0 tCO₂/ton to 1.94 tCO₂/ton for allocation purposes, potentially converting negative adjustment factors (indicating structural allowance deficits) into positive positions approaching the +3% regulatory ceiling.

Second, DCC holders gain temporal priority in allowance pre-allocation scheduling. Standard protocols distribute 70% of annual allowances upfront in January, with remaining 30% settled post-verification in the following year after actual emissions are confirmed [27]. This timing spread creates liquidity asymmetry where enterprises face immediate compliance costs while awaiting final allocation adjustments. High-grade DCC holders demonstrating consistent reporting quality and investment in monitoring infrastructure receive 90-95% initial allocation, unlocking significant liquidity advantages. Earlier allowance receipt enables strategic price arbitrage, selling excess permits during high-demand periods rather than accepting distressed prices during year-end compliance rushes. Allowance collateral financing becomes viable earlier in fiscal years when banks assess portfolio values. Compliance cost hedging through forward contracts requires upfront allowance possession that standard 70% allocation delays.

Third, DCC credentials can convert into China Certified Emission Reduction (CCER) credits under expedited methodology approval for internal corporate decarbonization projects. Current regulations permit CCER offsetting up to 5% of compliance obligations, previously limited to renewable energy and forestry projects [28]. By designating enterprise-specific deep decarbonization initiatives (hydrogen direct reduction iron pilots, carbon capture integration, extreme energy efficiency upgrades exceeding sectoral benchmarks) as CCER-eligible through sector-specific accounting guidelines, DCC transforms into compliance instruments tradable on national carbon markets. The Ministry of Ecology and Environment possesses regulatory authority to issue such technical specifications without legislative amendment [29], creating implementation pathways faster than formal CCER methodology revision processes.

The fiscal arithmetic in China's institutional context operates through intertemporal accounting rather than immediate cash flows. Awarding additional free allowances theoretically reduces future auction revenue potential as the market transitions toward greater allocation through paid mechanisms. However, two countervailing dynamics restore fiscal equilibrium over policy cycles. First, supporting leading industrial exporters through enhanced allowance allocation stabilizes their domestic operations and preserves corporate income tax base. Preventing competitive decline under CBAM pressure maintains employment in strategic sectors and avoids social instability costs exceeding foregone carbon revenue. Second, accelerated technological upgrading driven by DCC investment incentives enables progressively stricter future benchmark values [30]. Today's 3% allocation bonus facilitates capital formation for efficiency improvements that justify tomorrow's 10% benchmark tightening, creating a dynamic ratchet mechanism. The system progressively decarbonizes while maintaining industrial competitiveness during transition periods, achieving environmental objectives through induced innovation rather than forced contraction.

4.2 Cross-Border Recognition: The α Coefficient Framework

CBAM's implementing regulation calculates compliance obligations through the formula: CBAM Payment = Import Volume × (E_Actual - E_Benchmark) × P_Carbon, where E_Actual represents declared embedded emissions per unit product, E_Benchmark indicates EU production average performance standards, and P_Carbon denotes prevailing EU ETS auction clearing prices [2]. The Conditional Emission Rate (CER) coefficient previously introduced [31] adjusts this baseline to account for jurisdictional carbon accounting methodology differences, modifying the formula to: Adjusted Payment = Volume × (E_Actual × CER - E_Benchmark) × P_Carbon.

The DCC recognition framework introduces a second adjustment layer through: Modified Payment = Volume × (E_Actual × CER × (1 - α × DCC_Discount) - E_Benchmark) × P_Carbon. The recognition coefficient α governs the extent to which verified implicit carbon costs reduce effective CBAM exposure. When α equals zero, implicit costs receive no acknowledgment, forcing full payment under standard formulas. When α equals unity, complete recognition nullifies CBAM liabilities equivalent to documented implicit expenditures, though this extreme scenario faces practical constraints discussed subsequently. Realistic negotiated values inhabit the interval α ∈ (0,1), determined through bilateral agreements or multilateral frameworks that balance environmental integrity maintenance against fairness considerations for countries with existing climate policies.

The discount term DCC_Discount normalizes enterprise-level DCC holdings against total CBAM obligations, calculated as: DCC_Discount = (DCC_Holdings_Value / Total_CBAM_Liability). This ratio prevents over-crediting scenarios where claimed implicit costs exceed actual border adjustment exposure. An enterprise holding €5 million in verified DCC facing €15 million CBAM obligations would calculate DCC_Discount = 0.333, generating partial rather than complete liability offset even under high α values.

Consider a detailed numerical example using China's aluminum sector. A producer exports 100,000 tons annually with actual embedded emissions of 10.5 tCO₂ per ton aluminum, reflecting coal-heavy electricity grids and older smelting technology, against an EU production benchmark of 6.8 tCO₂/ton representing best available techniques [32]. At a carbon price of €80 per ton ETS allowance, baseline CBAM liability under standard methodology calculates as: 100,000 tons × (10.5 - 6.8) tCO₂/ton × €80/tCO₂ = €29.6 million annually. Introducing a CER coefficient of 1.403 to account for China-EU methodological differences [31] increases adjusted exposure to: 100,000 × (10.5 × 1.403 - 6.8) × 80 = €41.57 million.

Now suppose the producer holds DCC credentials representing €8 million in verified fuel excise payments and contracted renewable energy procurement costs, documented through State Grid invoices and tax authority confirmation. With negotiated α = 0.35 representing conservative initial recognition, and DCC_Discount calculated as 8/41.57 = 0.192, the modified formula yields: Payment = 100,000 × (10.5 × 1.403 × (1 - 0.35 × 0.192) - 6.8) × 80 = €40.65 million. This generates €0.92 million in annual savings, representing 2.2% liability reduction.

While the percentage appears modest, several contextual factors merit consideration. First, absolute value matters significantly for capital-intensive sectors operating on sub-5% net margins. Second, α exhibits path dependence and upward trajectory potential. Initial recognition at conservative values (α = 0.25-0.35) during pilot phases establishes institutional precedent and verification infrastructure maturity, facilitating progressive increases toward α = 0.50-0.70 as compliance track records accumulate and trust deepens. Third, the mechanism creates positive reinforcement loops where DCC value appreciation incentivizes additional implicit carbon cost generation through voluntary fuel switching or renewable energy procurement, even absent regulatory mandates. Fourth, DCC holdings provide CBAM cost hedging functionality, reducing uncertainty around future liability calculations as policy parameters evolve.

The α coefficient itself emerges as dynamic equilibrium rather than fixed parameter, responding to verification technology improvements, penalty regime stringency, and information revelation during pilot implementations. A bilateral recognition agreement might specify α(t) = α₀ + β × Verification_Quality_Score(t) + γ × Years_Without_Major_Fraud, creating scheduled appreciation tied to demonstrated performance. This dynamic formulation aligns incentives for genuine infrastructure investment while maintaining environmental integrity through reversibility provisions if gaming behaviors emerge.

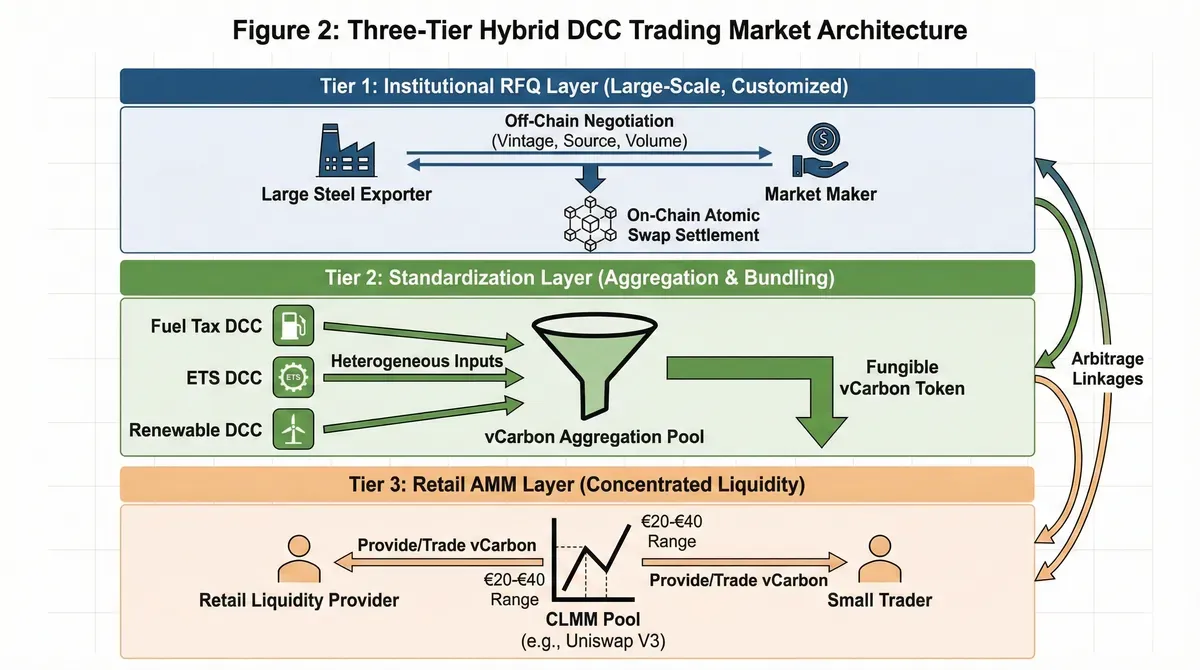

4.3 Secondary Market Trading: Conceptual Architecture

The market architecture presented here serves as a conceptual design space rather than a prescriptive implementation blueprint. Actual deployment would require extensive regulatory consultation, particularly regarding securities law classification, anti-money laundering compliance, and cross-border transaction governance. DCC secondary markets would serve enterprises lacking direct CBAM exposure but possessing implicit carbon cost credentials. An inland Chinese thermal power plant paying fuel consumption taxes generates DCC through documented expenditures yet faces no export obligations requiring CBAM compliance. Meanwhile, coastal aluminum smelters with substantial EU shipments require DCC for liability reduction but may have lower domestic tax burdens due to different energy consumption patterns or tax jurisdictions. Market mechanisms could bridge this mismatch, theoretically channeling DCC from generators to users through price discovery and liquidity provision.

However, DCC exhibits semi-fungible characteristics that complicate exchange design relative to homogeneous commodity markets. Unlike standardized products tradable through simple pricing mechanisms, individual DCC credentials carry distinct attributes affecting recognition value: source jurisdiction and its bilateral agreement status, underlying policy instrument type (fuel tax versus ETS cost versus renewable energy procurement), vintage year reflecting policy regime changes, and verification methodology rigor. EU recognition policies may differentiate among these dimensions. Fuel excise tax-derived DCC might achieve higher α recognition than renewable energy subsidy-based credentials due to verification simplicity and lower WTO subsidy classification risks.

This heterogeneity creates long-tail effects where specialized DCC categories suffer liquidity deficits. A 2023-vintage fuel tax DCC from India under initial bilateral pilot frameworks may hold different market value than 2026-vintage ETS allowance purchase DCC from China under mature recognition agreements, even though both theoretically represent equivalent implicit carbon costs. Vintage mismatch problems arise when policy regime transitions invalidate older credentials or modify conversion formulas. Price discontinuity manifests when EU regulatory announcements trigger stepwise DCC valuation adjustments, incompatible with smooth automated market maker curves designed for continuously variable asset prices.

The proposed three-tier hybrid structure addresses these complexities through functional layering. The base liquidity layer utilizes Concentrated Liquidity Market Makers (CLMM), pioneered by Uniswap V3 in decentralized finance contexts [33]. CLMM enables liquidity providers to concentrate capital deployment within specified price ranges rather than distributing uniformly across infinite intervals. For DCC markets, liquidity concentration within probable trading bands (€20-€40 based on implicit cost floors and α-discounted CBAM value ceilings) achieves capital efficiency potentially 4000× superior to constant product formulas that waste liquidity at unrealistic price extremes [34].

This efficiency matters critically for long-tail asset bootstrapping. DCC categories with monthly trading volumes under 1,000 units cannot attract professional market makers under traditional order book models requiring minimum depth commitments. CLMM allows retail liquidity providers to profitably participate despite low volumes by concentrating capital where trades actually occur. The base layer thus ensures even obscure DCC variants (Brazilian sugarcane ethanol subsidy credits, Turkish cement energy efficiency certificates) maintain discoverable prices, preventing market fragmentation that would undermine DCC fungibility.

The institutional transaction layer implements Request for Quote (RFQ) mechanisms for bulk transactions exceeding 10,000 ton-equivalent volumes. Large steel exporters requiring substantial DCC positions to optimize CBAM exposure across multiple product categories bypass AMM pools to avoid slippage that would occur when large orders exhaust concentrated liquidity ranges. Instead, they solicit competitive bids from designated market makers holding inventory positions and willing to quote firm prices for specific DCC attribute bundles. These quotes incorporate buyer requirements around vintage compatibility, verification standards, and delivery timing. Off-chain negotiation determines final pricing and terms, with on-chain settlement providing atomic swap guarantees preventing counterparty default.

RFQ systems prevent industrial-scale orders from destabilizing AMM pricing while providing precision matching impossible in algorithmic pools. When an aluminum producer needs 50,000 DCC units with 2025-2026 vintage from fuel tax sources in jurisdictions with α ≥ 0.30 recognition, broadcasting this demand into AMM pools would reveal proprietary compliance strategies and move markets adversely. RFQ confidentiality preserves information asymmetry while competitive bidding ensures efficient pricing.

The standardization layer introduces pooled tokens (vCarbon) aggregating heterogeneous DCC into composite instruments. Similar to mortgage-backed securities bundling diverse loans into tranched products differentiated by risk-return profiles, vCarbon packages multiple DCC vintages and source types into fungible units. A vCarbon token might represent a weighted basket: 40% Indian fuel tax DCC (2025-2026 vintage), 30% Chinese ETS allowance purchase DCC (2024-2025), 20% Brazilian renewable energy certificate DCC (2025), and 10% Turkish carbon tax DCC (2026). This composition rebalances quarterly based on recognition stability metrics and market depth indicators.

Retail participants trade standardized vCarbon on AMM pools without managing individual DCC attribute complexities. Sophisticated institutional players access granular DCC markets through RFQ when specific compliance requirements demand precise attribute matching. This layering partitions complexity along participant competence boundaries while maintaining overall market integration through arbitrage linkages between vCarbon and underlying DCC components.

Pricing models must account for regulatory arbitrage boundaries defining rational valuation ranges. DCC trades within corridors determined by implicit carbon cost generation floors and CBAM credit value ceilings. The floor reflects production costs: if fuel tax burdens embed €25/tCO₂ equivalent, sustained DCC pricing below this level signals either market dysfunction or changed tax policies invalidating original conversion formulas. Producers would cease DCC generation if sale proceeds fall below embedded costs. The ceiling derives from α-discounted CBAM credit value: when α = 0.35 and CBAM certificates trade at €80, DCC maximum rational price approaches €28 (0.35 × 80). Buyers would not pay above this threshold since cheaper CBAM certificate direct purchase becomes preferable.

Market equilibrium settles within this €25-€28 corridor through supply-demand dynamics. Tighter ranges indicate mature markets with stable recognition parameters and predictable future α trajectories. Wider ranges reflect uncertainty about bilateral negotiation outcomes, pending policy announcements, or verification disputes creating temporary dislocations. Risk premiums for fraud possibility and recognition revocation probability compress achievable prices below theoretical ceilings, with premium magnitude reflecting trust in issuing jurisdiction's governance quality and verification infrastructure robustness.

5. Preventing Gaming: Trust Without Surrender

DCC's evidential basis rooted in historical payment verification provides inherent fraud resistance absent in counterfactual-dependent mechanisms. Tax receipt authentication through government database integration eliminates the baseline construction and additionality determination challenges that plagued CDM. Nevertheless, three attack vectors require defensive architecture. First, tax documentation fabrication where entities forge payment records claiming non-existent contributions. Second, double-spending where identical tax payments generate multiple DCC issuances through coordinated submission across different verification nodes or time periods. Third, DCC laundering where credentials issued under lax standards or through corrupted verification processes enter circulation through secondary markets, contaminating the broader pool.

The primary defense layer embeds API integration with national tax authority systems. When an Indian enterprise submits fuel consumption data requesting DCC generation through the proposed DGFT portal, the validation engine queries the Goods and Services Tax Network and Central Board of Indirect Taxes and Excise databases [35]. Cryptographic signatures using TLS 1.3 mutual authentication ensure data integrity during transmission, preventing man-in-middle attacks or packet injection. The query structure includes GST registration number, tax assessment year identifier, specific invoice numbers claimed for DCC conversion, and payment transaction reference codes.

Response data returns matching tax liability records or null results if no corresponding payment exists in official registers. Only affirmative matches with cryptographic receipt signatures from tax authority servers trigger DCC minting approval. This architecture transforms fabrication attacks from document forgery exercises into nation-state-level database breach requirements, orders of magnitude harder than creating falsified paper receipts or manipulated spreadsheet records. An attacker would need to compromise both the requesting enterprise's private key infrastructure and the government tax authority's secure database systems simultaneously, a capability threshold exceeding typical corporate fraud resources.

Double-spending prevention employs smart contract burn mechanisms with cryptographic uniqueness enforcement. Each DCC token contains a unique identifier derived from the originating tax transaction hash combined with enterprise identity and timestamp. The generation function calculates: DCC_ID = Hash(Tax_Transaction_ID || Enterprise_Public_Key || Timestamp || Nonce). Upon CBAM submission or secondary market sale, the DCC contract executes a burn operation, permanently removing the token from circulation and recording the consumption event in an append-only blockchain ledger. Subsequent attempts to reference the same underlying tax receipt for new DCC generation fail at the uniqueness check, as the consumed DCC_ID already appears in the global registry accessible to all verification nodes.

This approach differs fundamentally from traditional carbon offset registries that rely on centralized databases and trusted intermediaries with manual reconciliation. Blockchain's distributed consensus and cryptographic hash functions provide mathematical certainty that spent DCC cannot re-enter circulation without detectable tampering requiring simultaneous compromise of threshold validator nodes (three of five in the proposed architecture). Even sophisticated attackers controlling individual verification nodes cannot unilaterally double-spend without detection, as the required multi-signature threshold and cross-node gossip protocols ensure inconsistency detection within consensus latency periods (typically under 10 seconds for permissioned blockchains).

DCC laundering poses subtler challenges related to verification standard divergence across jurisdictions. Suppose a country with inadequate tax administration or captured regulatory agencies issues dubious DCC through rubber-stamp approval processes. These questionable credentials subsequently trade to legitimate buyers who unknowingly acquire contaminated holdings. If these DCC achieve CBAM recognition before fraud discovery, systemic integrity suffers reputational damage affecting even properly issued credentials. The defense strategy implements source metadata requirements and selective recognition filters.

Each DCC token encodes comprehensive provenance data: policy instrument classification from a standardized taxonomy (fuel excise, ETS allowance, renewable energy procurement), issuing authority with ISO 3166 country codes and government agency identifiers, verification methodology with version numbers and compliance standard references (ISO 14064, GHG Protocol, national accounting frameworks), and audit trail hashes from each validation step. EU CBAM authorities or enterprises performing due diligence can establish whitelist filters accepting only DCC meeting specified criteria. For example, a filter might accept fuel tax-based DCC from jurisdictions with World Bank governance indicators above specified thresholds while rejecting renewable energy subsidy DCC due to higher verification complexity and WTO subsidy concerns.

This selective recognition mechanism creates compliance quality hierarchies without blanket jurisdiction exclusion that would trigger diplomatic backlash. High-quality issuers with demonstrated verification rigor and clean audit records gain broad acceptance across buyer pools and higher α recognition coefficients. Intermediate cases with adequate but unproven systems face partial recognition through discounted α values (perhaps 0.20 versus 0.35 for premium jurisdictions) pending track record establishment. Inadequate systems receive zero recognition until governance reforms materialize, creating powerful incentives for institutional improvement. The gradient approach rewards excellence while enabling participation, avoiding the binary inclusion-exclusion dynamics that characterized CDM and created resentment.

Macro-reconciliation provides final assurance through aggregate data consistency checks. Periodic audits compare cumulative DCC issuance volumes against national fiscal statistics published in government budget documents and IMF Article IV consultation reports [36]. If a country's total fuel tax-based DCC generation exceeds actual fuel tax revenue collected during corresponding periods, systematic fraud has likely occurred. The discrepancy triggers enhanced scrutiny including on-site inspections, temporary recognition suspension for new issuances pending investigation resolution, and potential retroactive CBAM liability adjustments requiring purchasers of invalidated DCC to settle shortfalls.

This mechanism functions analogously to balance-of-payments accounting where impossible capital flow figures reveal measurement failures or deliberate misreporting. The analogy extends to enforcement: just as IMF program conditionality can require fiscal data transparency improvements, DCC recognition agreements could stipulate audit access rights and statistical disclosure requirements as participation conditions. Countries valuing DCC market access would face strong incentives for data integrity maintenance, creating self-enforcing compliance through market discipline rather than relying solely on ex-post penalties.

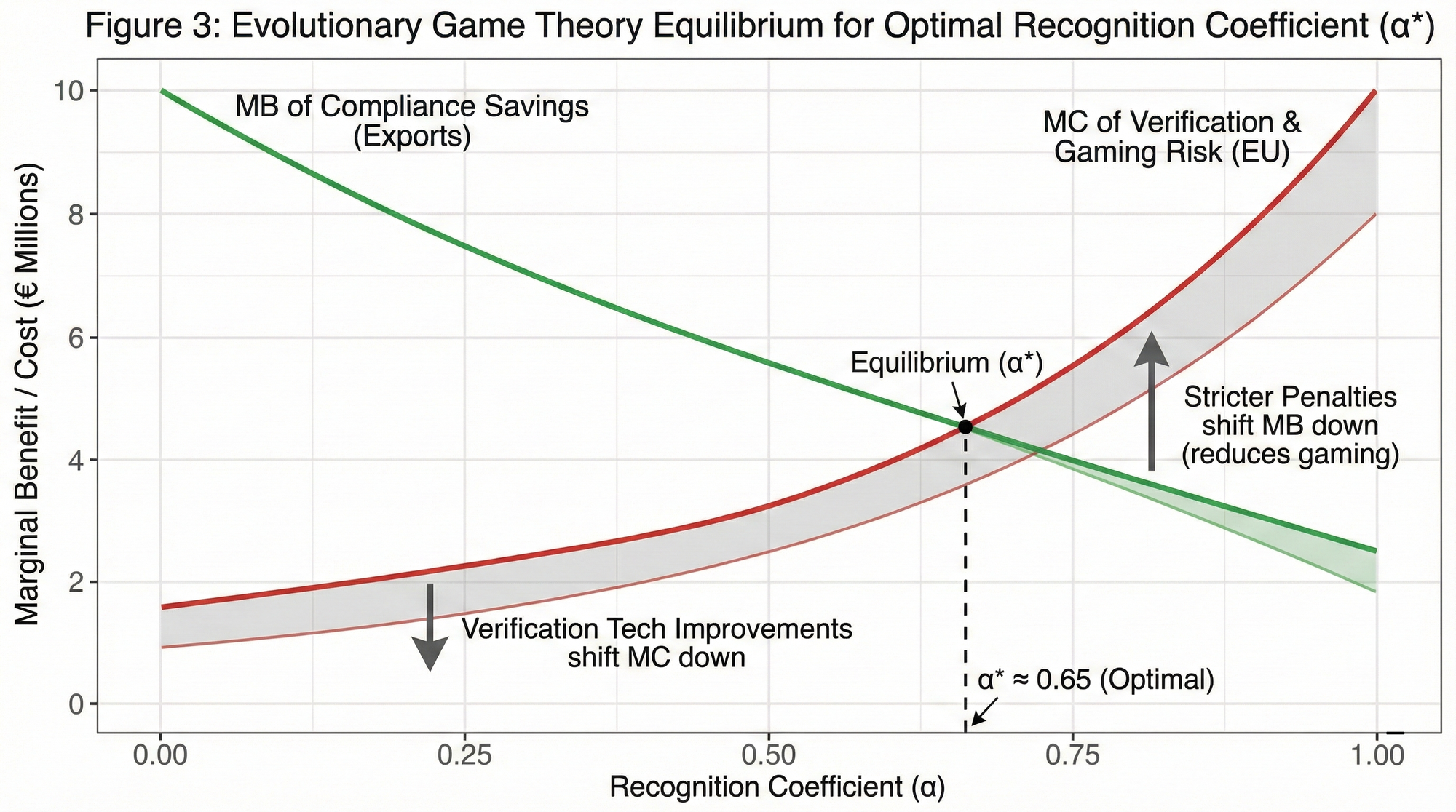

6. Evolutionary Game Theory: The α Recognition Equilibrium

Recognition coefficient α emerges from strategic interaction between the EU maintaining CBAM environmental integrity and Global South countries seeking acknowledgment for existing climate policies. Formalizing this as a two-player evolutionary game reveals equilibrium properties and stability conditions. The EU selects α ∈ [0,1], while exporting nations choose between genuine MRV infrastructure investment or reporting manipulation strategies. Payoff structures shape equilibrium selection through asymmetric costs and benefits.

For exporting countries, genuine infrastructure investment generates CBAM cost reduction equal to: Savings = Export Volume × Emission Intensity × Carbon Price × α × (Verified Implicit Price / Carbon Price), minus upfront deployment costs C_Investment for tax system API integration, blockchain node operation, and auditor training. Using the Chinese aluminum example from Section 4.2, an enterprise exporting 100,000 tons faces baseline CBAM exposure of €41.57 million. With α = 0.35 and verified implicit costs of €8 million (DCC_Discount = 0.192), annual savings reach €0.92 million. If C_Investment totals €2 million for system setup, the payback period extends approximately 2.2 years, acceptable for long-term export operations but challenging for marginal producers or those facing market uncertainty.

Manipulation attempts yield similar nominal savings without infrastructure costs but carry detection probability p_Penalty × expected sanctions F_Penalty. If detection occurs through macro-reconciliation audits or whistleblower reports, penalties could include: confiscation of CBAM certificate value represented by fraudulent DCC (€0.92 million in the example), suspension of recognition privileges for three years forcing reliance on expensive default values, and reputational damage affecting financing costs and market access. Setting p_Penalty = 0.15 (reasonably high given tax authority data availability) and F_Penalty = €5 million (3× single-year savings plus recognition suspension costs), expected manipulation cost reaches €0.75 million, making genuine investment the dominant strategy for risk-averse actors.

When α = 0, this calculus collapses. Investment returns zero because no recognition occurs regardless of verification quality, creating classic prisoner's dilemma dynamics where rational actors choose non-participation. Without CBAM credit value, enterprises lack incentives for costly DCC infrastructure deployment. Countries face domestic political resistance to transparency measures when no international benefit materializes. The system remains stuck at zero-investment equilibrium even though cooperative solutions would improve all parties' welfare. Current CBAM implementation without implicit cost recognition mechanisms manifests precisely this inefficient outcome [37].

When α = 1, complete recognition enables maximal manipulation incentives. If fraudulent DCC receives full CBAM credit equal to verified credentials, sophisticated gaming strategies become profitable despite detection risks. A country could systematically overstate fuel tax rates in reported statistics, generate excess DCC relative to actual payments, and capture CBAM savings exceeding true implicit costs. Detection probability would need to approach certainty (p_Penalty → 1) to deter such behavior, requiring surveillance resources incompatible with sovereignty principles and administrative feasibility. Environmental integrity collapses as verification shortcuts proliferate and baseline inflation mirrors CDM's additionality gaming.

Optimal α* emerges where marginal benefits of increased recognition equal marginal costs from verification requirements and gaming vulnerabilities. Mathematically, this equilibrium satisfies: ∂(Expected Savings + Verification Cost + Gaming Damage) / ∂α = 0. Several structural factors shift this optimum. Verification technology improvements reduce required α levels to achieve target participation rates. If blockchain-based tax APIs slash verification costs by 80% relative to manual audit methods, the EU can confidently raise α from 0.25 to 0.40 while maintaining fraud risk below acceptable thresholds (perhaps 5% expected leakage) [38].

Penalty severity exhibits positive correlation with sustainable α values. Stringent sanctions including 30% of CBAM liability surcharges plus multi-year recognition suspension deter gaming more effectively than nominal fines that rational violators treat as cost of doing business. This creates policy complementarity: countries implementing harsh penalties for DCC fraud can credibly negotiate higher α recognition because verification confidence increases. Conversely, weak enforcement regimes face α discounts reflecting elevated gaming risk.

Initial carbon pricing levels in exporting countries inversely correlate with trust-building periods required. Nations operating mature ETS markets with decade-long verification infrastructure and established third-party auditor industries warrant higher initial α values (perhaps 0.30-0.35) than jurisdictions lacking carbon pricing experience where verification capacity must develop from zero baseline. This differentiation avoids one-size-fits-all approaches that either under-credit advanced reformers or over-trust weak-capacity states. A tiered recognition schedule might specify α_Tier1 = 0.35 for countries with operating ETS, α_Tier2 = 0.25 for countries with comprehensive fuel taxation, and α_Tier3 = 0.15 for countries with nascent climate policies, subject to upward revision as capacity improves.

Information asymmetry fundamentally constrains feasible α ceilings even under perfect verification. The EU cannot directly observe true implicit carbon costs, relying instead on reported data subject to strategic manipulation. Optimal tariff theory under asymmetric information suggests taxing slightly above calculated equivalence to compensate for uncertainty [39]. Translated into DCC context, prudent α might settle at 0.60-0.75 rather than unity even when verification technology approaches perfect accuracy, maintaining safety margins against systematic bias in implicit cost calculations or coordinated misreporting beyond individual verification node detection capabilities.

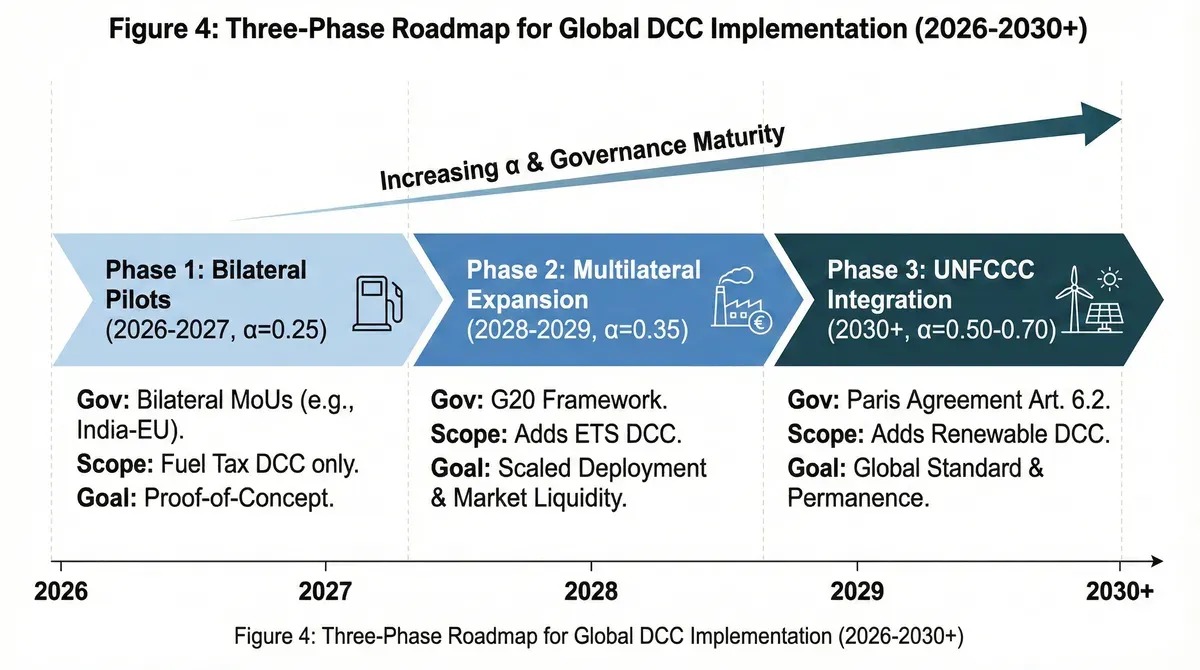

7. Three-Phase Roadmap: From Pilots to Protocols

Phase 1 (2026-2027): Bilateral Pilots at α = 0.25

Initial deployment targets three jurisdictions selected for heterogeneous industrial profiles and existing climate policy frameworks: India's established fuel taxation and RoDTEP infrastructure, Brazil's biofuel mandate creating implicit renewable energy costs, and Turkey's position bridging OECD membership with developing economy characteristics. Scope restriction limits recognition to fuel excise tax-derived DCC exclusively, excluding renewable energy subsidies and energy efficiency standards that pose greater verification challenges and WTO subsidy classification uncertainties [40].

Negotiation occurs through bilateral Memoranda of Understanding rather than multilateral WTO processes, accelerating implementation by circumventing consensus requirements among 164 members. These MoUs establish technical parameters: conversion formulas translating tax payments into DCC units, verification procedures including API specifications and audit protocols, and α coefficient starting values with scheduled review milestones. The agreements include sunset clauses activating after 24 months, requiring explicit renewal based on performance assessment and fraud incident review. This reversibility provision reduces political resistance while maintaining credible commitment to environmental integrity.

India's participation leverages existing Directorate General of Foreign Trade digital infrastructure, requiring incremental ICEGATE system modifications to validate DCC submissions rather than ground-up platform construction [41]. The technical lift involves API development connecting ICEGATE to GST Network databases, DCC credential schema definition compatible with W3C standards, and blockchain node deployment using existing National Informatics Centre data centers. Estimated deployment cost reaches ₹150 crore (approximately €16 million) covering software development, cybersecurity hardening, and verifier training programs, manageable within normal customs modernization budgets.

Brazil's biofuel taxation regime offers alternative DCC generation pathways beyond fossil fuel excise. The RenovaBio program mandates blending targets creating implicit carbon costs through Decarbonization Credit (CBIO) purchases required by fuel distributors [42]. Converting CBIO expenditures into DCC credentials requires methodology development addressing vintage compatibility and additionality concerns (ensuring credits represent marginal biofuel expansion rather than baseline compliance). This methodological complexity justifies Brazil's inclusion despite adding technical challenges, as successful resolution expands DCC applicability beyond simple fuel taxes.

Turkey's participation tests DCC resilience across governance contexts. As OECD member with EU accession candidacy, Turkey maintains higher institutional quality than typical developing countries while facing similar CBAM pressure on steel and cement exports. Its nascent ETS development provides pilot opportunities for allowance-purchase-based DCC, informing future Chinese integration. Geographic proximity to EU facilitates regulatory dialogue and reduces cultural translation costs in MoU negotiation.

The α = 0.25 threshold represents conservative calibration reflecting pilot uncertainties rather than optimized equilibrium. With verification protocols untested at scale and fraud detection mechanisms relying on unproven macro-reconciliation procedures, the EU prudently limits exposure. This initial value captures approximately one-quarter of verified implicit costs, generating meaningful enterprise savings (€230,000 for the Chinese aluminum example) while maintaining substantial CBAM revenue flows and environmental integrity buffers. Successful Phase 1 execution requires demonstrating zero major fraud incidents across 100+ participating enterprises, establishing empirical foundations for expanded recognition.

Phase 2 (2028-2029): Multilateral Expansion at α = 0.35

Transition to G20 Climate Finance Working Group negotiation provides elevated forum and broader participant base beyond bilateral pioneers [43]. Coverage expands to include carbon market costs, specifically ETS allowance purchases and carbon tax payments meeting criteria: auction-determined pricing ensuring market mechanisms rather than administrative fiat, independent verification per ISO 14065 standards providing third-party assurance, and public transaction registries enabling civil society monitoring. This expansion recognizes explicit carbon pricing mechanisms while maintaining verification rigor through established standards.

The α increase from 0.25 to 0.35 reflects accumulated confidence from pilot performance metrics plus verification cost reductions through scaled deployment. Digital MRV infrastructure deployed during Phase 1 achieves economies of scale, reducing per-enterprise validation expenses from initial €45,000 to approximately €12,000 through automation gains and standardized procedures [44]. Enhanced penalty frameworks implemented following Phase 1 lessons learned increase expected sanctions for non-compliance, deterring marginal gaming attempts that might proliferate under broader participation. Detection probability improves as macro-reconciliation databases accumulate multi-year time series enabling statistical anomaly detection.

Participation scales from initial three countries to approximately fifteen jurisdictions, incorporating China's expanded national ETS sectors (steel, cement, aluminum joining power generation), additional BRICS members (South Africa, Indonesia), and select middle-income economies with material CBAM exposure (Mexico, Malaysia, Thailand). Market infrastructure matures with DCC secondary trading volumes reaching €800 million-€1.2 billion annually based on 10-15 million ton-equivalent annual issuance at average €60-€80 valuations, establishing liquid pricing benchmarks and reducing enterprise hedging costs through derivatives availability.

Phase 2 duration extends 18-24 months rather than fixed calendar period, allowing natural evolution pacing tied to institutional capacity rather than arbitrary deadlines. Transition to Phase 3 requires meeting objective criteria: cumulative DCC issuance exceeding 20 million ton-equivalent, fraud incident rates below 2% of volume, and successful WTO challenge resolution if any member initiates subsidy complaints. These gating mechanisms ensure Phase 2 stability before committing to deeper integration.

Phase 3 (2030+): UNFCCC Integration at α = 0.50-0.70

Institutionalization occurs through Article 6.2 cooperative approaches framework under the Paris Agreement, embedding DCC recognition into international climate law rather than bilateral trade agreements [45]. This transition provides permanence and multilateral legitimacy while subjecting DCC to UNFCCC governance including Article 6 Supervisory Body oversight. Coverage expands cautiously to renewable energy subsidies meeting stringent third-party audit requirements specified in Article 6.2 guidance, addressing historical exclusion of policy instruments creating substantial implicit costs but requiring complex verification methodologies.

The α band (0.50-0.70) accommodates jurisdictional variation based on demonstrated track records. Countries with decade-long DCC programs, zero material fraud incidents, and robust domestic enforcement achieve 0.70 maximum recognition, providing substantial CBAM relief while maintaining 30% minimum payment ensuring continued environmental integrity. Recent adopters with adequate but unproven systems receive 0.50 pending reliability demonstration over 3-5 year probationary periods. This tiered approach creates performance incentives while avoiding excessive rigidity that would prevent participation.

Market maturity indicators guide Phase 3 entry triggers beyond calendar milestones. DCC issuance volumes must reach minimum 20 million tCO₂-equivalent annually across participating countries, ensuring sufficient market depth for price discovery and liquidity provision [46]. Secondary market capitalization should exceed €4-€6 billion with bid-ask spreads consistently below 3%, signaling efficient allocation mechanisms attractive to institutional participants. Resolution of at least two WTO dispute cases involving DCC-related complaints without adverse subsidy rulings confirms legal robustness under international trade law.

Governance transitions from EU-dominated bilateral negotiations to truly multilateral oversight. The Article 6 Supervisory Body, comprising representatives from all regional groups with decisions requiring qualified majorities, assumes primary regulatory authority for DCC methodology approval and recognition standard setting. This shift acknowledges DCC evolution from European regulatory accommodation to global climate finance infrastructure requiring governance structures representing broader stakeholder constituencies beyond carbon importers.

7.5 Limitations and Future Research Directions

This study acknowledges several constraints requiring future investigation. First, the fiscal closed-loop analysis assumes stable tax policy environments where fuel excise rates remain constant or increase gradually. Abrupt government decisions to reduce diesel taxes for inflation relief or restructure carbon taxation during energy crises could invalidate DCC generation formulas, requiring dynamic adjustment mechanisms not fully specified here. The framework needs automatic recalibration protocols responding to policy changes while preventing retroactive value destruction for existing DCC holdings, perhaps through vintage-specific conversion ratios that lock initial issuance parameters.

Second, the α coefficient optimization relies on game-theoretic equilibrium assumptions that may oversimplify real-world negotiation dynamics involving multiple stakeholders, domestic political constraints, and path-dependent institutional commitments. Actual bilateral negotiations incorporate factors beyond verification costs and fraud risks: geopolitical relationships, trade balance considerations, domestic industrial lobbying, and climate justice narratives. Future research should employ agent-based modeling incorporating these political economy dimensions rather than purely rational-actor frameworks, potentially revealing equilibria inaccessible through current analytical approaches.

Third, our market architecture proposals draw extensively from decentralized finance innovations (CLMM, RFQ hybrid models) without comprehensive regulatory mapping. Securities law classification of DCC tokens remains ambiguous across jurisdictions. Depending on specific design choices, DCC might constitute commodities subject to futures trading regulations, securities requiring prospectus registration and investor protection compliance, or hybrid instruments facing overlapping regulatory regimes. Whether DCC trading platforms require exchange licenses, how cross-border transactions interface with capital controls, and what investor suitability standards apply all remain unresolved. Pilot implementations must prioritize regulatory clarity through formal determination processes before scaled deployment to avoid legal challenges that could invalidate accumulated DCC positions.

Fourth, distributional effects across firm sizes require deeper analysis. Large enterprises with dedicated compliance teams, established relationships with accredited verifiers, and sophisticated digital infrastructure may capture disproportionate DCC benefits compared to small and medium enterprises lacking technical capacity for blockchain integration and standardized tax documentation. Transaction costs for API development, auditor engagement, and marketplace participation might exceed DCC value for smaller exporters, creating de facto exclusion despite formal program openness. Policy designs ensuring equitable participation through aggregation mechanisms (industry association platforms pooling SME credentials) or subsidized technical assistance merit future research and pilot testing.

Fifth, empirical validation relies primarily on Tata Steel's detailed case study. While this provides operational depth and quantified benefit calculations, breadth expansion across multiple sectors (cement production, aluminum smelting, chemical manufacturing, fertilizer production) and jurisdictions (Brazilian ethanol, Turkish ceramics, Indonesian palm oil) would strengthen generalizability claims. The 2026-2027 pilot phase offers opportunities for rigorous quasi-experimental evaluation designs, measuring actual CBAM liability reductions, compliance cost changes relative to control groups, and unintended market distortions such as DCC hoarding or speculative price manipulation.

Future research should pursue four complementary directions. First, experimental economics laboratory studies testing α recognition thresholds through simulated bilateral negotiations could identify optimal starting values balancing trust-building requirements and meaningful incentive provision. Behavioral experiments with real monetary stakes involving trade negotiators and climate policy experts might reveal willingness-to-accept and willingness-to-pay schedules for recognition coefficient changes, informing actual diplomatic strategies.

Second, legal scholarship analyzing WTO compatibility under the Agreement on Subsidies and Countervailing Measures Article 1 (subsidy definition requiring financial contribution and benefit conferral) and Article 3 (prohibited export subsidies) would clarify permissible design boundaries. Detailed analysis comparing GEL's regulatory velocity provision to traditional export subsidies, examining whether reduced customs processing constitutes financial contribution, and assessing specificity tests could prevent future trade disputes derailing DCC implementation.

Third, cybersecurity and technology assessments evaluating API integration vulnerabilities, blockchain consensus attack vectors, and system resilience under adversarial conditions inform implementation feasibility. Penetration testing simulating tax database breach attempts, double-spending attacks, and verification node compromise scenarios would quantify security risks and necessary defensive investments, preventing catastrophic failures during operational deployment.

Fourth, longitudinal econometric studies tracking α evolution trajectories post-pilot using difference-in-differences or synthetic control methods provide empirical grounding for theoretical phase transition predictions. Comparing countries entering Phase 2 with different initial α values, fraud incident rates, and verification infrastructure investments could validate or refute game-theoretic models predicting equilibrium convergence, informing refinements to recognition coefficient formulas.

8. Conclusion: From Cost to Asset Through Accounting Infrastructure

Digital Cost Certificates provide a standardized accounting interface addressing a specific technical gap in current carbon border adjustment mechanisms: the absence of protocols for verifying and recognizing implicit carbon costs in compliance calculations. By certifying historical policy expenditures through tax authority database integration rather than promising future reductions requiring baseline construction, DCC sidesteps the verification challenges that destroyed CDM and VCM credibility. The mechanism operates within CBAM's existing structure, offering a complementary layer subject to negotiated recognition parameters rather than demanding regulatory redesign.

The framework's architecture achieves fiscal neutrality through asymmetric value creation. Governments retain tax revenues while providing regulatory efficiency gains (customs acceleration, allowance allocation timing) costing virtually nothing at margin. Enterprises monetize 15-35% of stranded implicit costs through velocity conversion and liquidity improvements, transforming dead weight into productive value. This economic structure enables climate policy advancement without fiscal drain, addressing developing country constraints that limit green subsidy deployment.

Recognition coefficient α requires careful calibration balancing trust-building through conservative initial values against meaningful incentive provision through progressive increases. Our three-phase roadmap provides temporal structure, allowing proof-of-concept validation before scaled commitment. Success metrics emphasize fraud prevention below 2% thresholds and verification cost reduction achieving €12,000 per enterprise through automation, the twin foundations of sustainable DCC legitimacy alongside environmental integrity maintenance.

The path forward demands parallel advancement across multiple dimensions: technical infrastructure deployment including API integration and blockchain node operation, legal framework development clarifying securities classification and WTO compliance, institutional capacity building training verifiers and auditors in new methodologies, and diplomatic negotiation establishing bilateral then multilateral recognition agreements. No single dimension suffices; coordination failures could derail implementation despite technical feasibility.

Future research should quantify α optimization through experimental economics, testing recognition thresholds that maximize developing country participation while satisfying environmental integrity constraints. Empirical validation using actual CBAM declaration data commencing January 2026 will calibrate theoretical models against operational reality, identifying gaps between designed and emergent behaviors. Legal analysis mapping WTO subsidy definitions onto DCC characteristics would prevent compliance challenges invalidating accumulated credentials. Technology assessments evaluating cybersecurity vulnerabilities inform defensive investment requirements.

DCC offers developing nations an accounting mechanism for climate policy costs already incurred, converting compliance burden into documented contributions toward decarbonization objectives. By providing this recognition interface, the framework enables structured negotiation around appropriate credit levels, verification standards, and discount factors rather than leaving implicit costs completely unacknowledged. Whether α settles at 0.25, 0.50, or 0.70 matters less than establishing the principle that verifiable policy expenditures merit systematic consideration within international carbon pricing architectures. The framework transforms what is currently an accounting void into negotiable territory, advancing both climate justice and environmental integrity through careful institutional design.

References

[1] Petroleum Planning and Analysis Cell. (2024). Central and State Tax on Petrol and Diesel in India. Government of India. https://cleartax.in/s/petrol-and-diesel-tax

[2] European Commission. (2023). Commission Implementing Regulation (EU) 2023/1773 laying down the rules for the application of Regulation (EU) 2023/956 as regards reporting obligations for the purposes of the carbon border adjustment mechanism during the transitional period. Official Journal of the European Union, L228/1-164.

[3] Internal Offset Mechanism (IOM) Institutional Design and Fiscal Closed-Loop Verification Research Report. (2026). Tata Steel Limited Case Study Analysis. Terawatt Times Institute Working Paper, Houston, TX.

[4] Streck, C., Keenlyside, P., & von Unger, M. (2016). The Paris Agreement: A New Beginning. Journal for European Environmental & Planning Law, 13(1), 3-29.

[5] UNFCCC. (2015). CDM Methodology Booklet (Ninth Edition). United Nations Framework Convention on Climate Change, Bonn. https://cdm.unfccc.int/methodologies/

[6] West, T.A.P., Wunder, S., Sills, E.O., Börner, J., Rifai, S.W., Neidermeier, A.N., Kontoleon, A., & Soest, D. (2023). Action needed to make carbon offsets from forest conservation work for climate change mitigation. Science, 381(6660), 873-877.

[7] Ecosystem Marketplace. (2024). State of the Voluntary Carbon Markets 2023: Market in Transition. Forest Trends Association, Washington, DC.

[8] Government of India. (2024). State-wise VAT/Sales Tax Rates on Petroleum Products. Ministry of Petroleum and Natural Gas, New Delhi. https://ppac.gov.in/prices/vat-sales-tax-gst-rates

[9] Goods and Services Tax Network. (2024). GST System Architecture and Data Security Protocols. Government of India. https://www.gstn.org.in/

[10] Mehling, M.A., van Asselt, H., Das, K., Droege, S., & Verkuijl, C. (2019). Designing Border Carbon Adjustments for Enhanced Climate Action. American Journal of International Law, 113(3), 433-481.

[11] World Trade Organization. (2024). Dispute Settlement Activity: Adjudication Statistics. https://www.wto.org/english/tratop_e/dispu_e/dispustats_e.htm

[12] W3C. (2022). Verifiable Credentials Data Model v2.0. World Wide Web Consortium. https://www.w3.org/TR/vc-data-model-2.0/

[13] IPCC. (2006). 2006 IPCC Guidelines for National Greenhouse Gas Inventories, Volume 2: Energy. Intergovernmental Panel on Climate Change, Geneva.

[14] Government of India. (2023). Foreign Trade Policy 2023. Directorate General of Foreign Trade, Ministry of Commerce and Industry, New Delhi. https://www.dgft.gov.in/

[15] Ministry of Commerce and Industry. (2024). RoDTEP Scheme: Rates and Procedures. Government of India. https://www.dgft.gov.in/CP/?opt=RoDTEP

[16] Boneh, D., Lynn, B., & Shacham, H. (2001). Short Signatures from the Weil Pairing. In C. Boyd (Ed.), Advances in Cryptology—ASIACRYPT 2001 (pp. 514-532). Springer, Berlin.

[17] Stratrich Consulting. (2023). An Overview of India's Foreign Trade Policy 2023: Transition to Remission-based Export Support. https://stratrich.com/insights/an-overview-of-indias-foreign-trade-policy-2023/

[18] A2Z Tax Corp. (2024). Steel Sector Exclusion from Export Incentive Schemes: Budgetary and WTO Considerations. https://a2ztaxcorp.net/interest-subvention-list-of-eligible-items-unlikely-to-be-extended-immediately/

[19] Press Information Bureau. (2023). Union Minister Inaugurates Direct Port Entry Facility at V.O. Chidambaranar Port. Government of India, Ministry of Ports, Shipping and Waterways. https://www.pib.gov.in/PressReleasePage.aspx?PRID=1667782

[20] Cogoport. (2024). Impact Assessment of India's Direct Port Delivery Initiative on Export Logistics Efficiency. https://www.cogoport.com/blogs/direct-port-delivery

[21] Authorized Economic Operator Programme India. (2024). Benefits Associated with AEO Tier-3 Certification. Central Board of Indirect Taxes and Customs. https://aeoindia.gov.in/SourceCode/Website/t3.php

[22] Indian Customs Electronic Gateway. (2024). ICEGATE System Architecture and API Documentation. https://www.icegate.gov.in/

[23] Jawaharlal Nehru Port Trust. (2024). Direct Port Delivery and Direct Port Entry: Cost-Benefit Analysis for Stakeholders. https://www.cybex.in/exim-news/jnpt-highlights-the-importance-of-12607

[24] Fortune India. (2024). Steel Industry Pricing Dynamics and Market Outlook. https://www.fortuneindia.com/long-reads/the-brief-the-steel-dilemma/109960

[25] GuruFocus. (2024). Tata Steel Limited Financial Analysis: Weighted Average Cost of Capital. https://www.gurufocus.com/term/wacc/NSE:TATASTEEL

[26] Ministry of Ecology and Environment. (2024). Notice on the Total Amount Setting and Allocation Plan for Carbon Emission Allowances in the National Carbon Emissions Trading Market for the Steel, Cement, and Aluminum Industries (2024-2025). People's Republic of China. https://www.mee.gov.cn/

[27] International Carbon Action Partnership. (2024). China Releases 2024-2025 Allowance Allocation Plan for Industrial Sectors in National ETS. https://icapcarbonaction.com/en/news/china-releases-2024-2025-allowance-allocation-plan-industrial-sectors-national-ets

[28] International Carbon Action Partnership. (2024). China National Emissions Trading System: Policy Design Features and Updates. https://icapcarbonaction.com/en/ets/china-national-ets

[29] National People's Congress. (2024). Interim Regulations on the Administration of Carbon Emissions Trading. Standing Committee of the National People's Congress, People's Republic of China.

[30] Ministry of Ecology and Environment. (2024). Progress Report of China's National Carbon Market 2024. People's Republic of China. https://www.mee.gov.cn/ywdt/xwfb/202407/W020240722528850763859.pdf

[31] Conditional Amplification in CBAM Compliance: The Φ-Ψ-τ Framework for Understanding National Capability and Product Complexity Interactions. (2025). Terawatt Times Institute Research Paper Series, Article A7.

[32] International Aluminium Institute. (2023). Global Aluminium Cycle: Production and Emissions Benchmarking Report 2023. London, UK.