The Four Blind Spots of CBAM: Why Nearly €90 Billion in Global Trade Needs a New Framework

The EU CBAM's demand for uniform carbon metrics creates four structural blind spots: a recognition gap, a clean production paradox, ignored development differences, and design rigidity. This article proposes a 3-step translation-enhanced reform to restore carbon tradability.

Abstract

The European Union's Carbon Border Adjustment Mechanism entered its definitive phase on January 1, 2026. Covering approximately €89 billion in annual imports and 260 million tonnes of embedded CO₂ emissions, CBAM attempts to prevent carbon leakage by extending EU carbon pricing to imported goods. The mechanism achieves this narrow legal objective through administrative simplicity, applying uniform emission benchmarks and default values regardless of the exporting country's industrial structure, carbon governance architecture, or developmental context. The broader legitimacy claim, which is that CBAM represents a fair contribution to global decarbonization, rests on four structural blind spots that the transitional period has rendered visible.

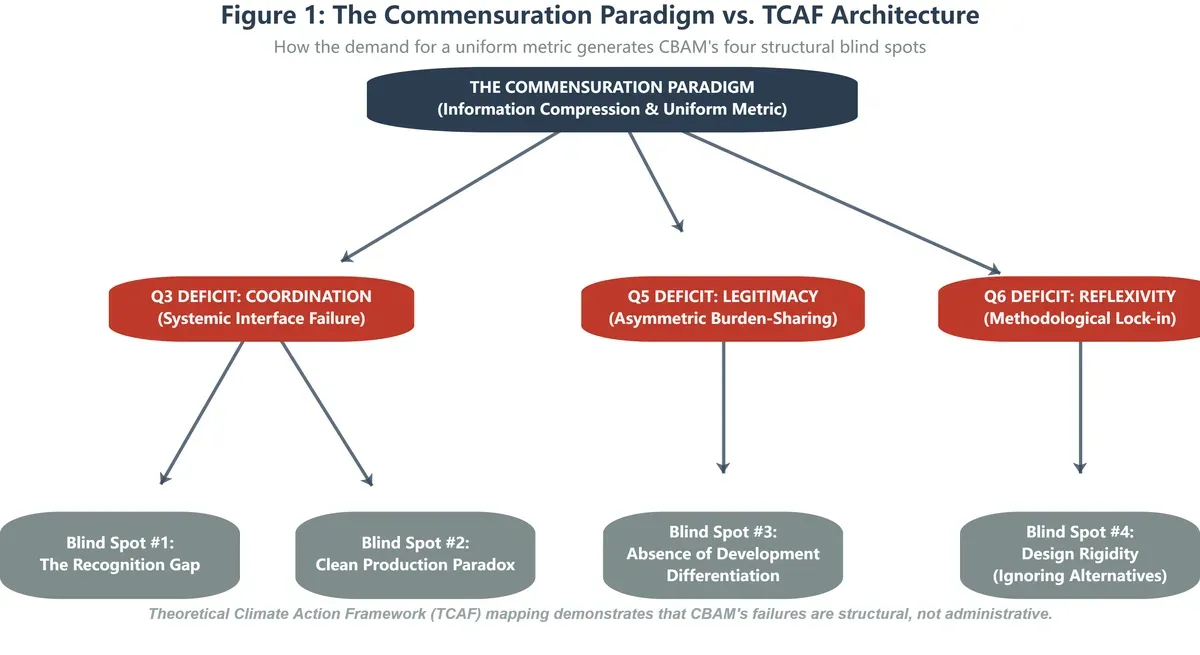

This paper identifies and analyzes those blind spots. The first is a recognition gap that operates through three distinct mechanisms: implicit instruments (differential electricity pricing, fuel excise, biofuel credits) that impose real carbon-linked costs but fall outside Article 9's eligibility criteria; explicit carbon markets whose allocation design reduces Article 9's effective carbon price to a small fraction of the nominal market clearing price; and definitional incompatibilities at the unit level that prevent bilateral reconciliation even in principle. The second is a clean production paradox that withholds credit both from low-emission producers in jurisdictions without explicit carbon pricing and from frontier performers in jurisdictions whose intensity-based carbon markets reward efficiency through surplus allocation rather than deficit purchase. The third is the absence of development differentiation, which applies uniform rules across fundamentally asymmetric administrative and economic contexts and creates an adjustment window that favors EU producers over foreign producers with equivalent or better emission performance. The fourth is design rigidity, visible in the contrast between CBAM's commensuration-based template and the alternative mechanisms now entering legislative pipelines in the United Kingdom, the United States, and Canada.

These four failures share a structural origin in what we term the commensuration paradigm, which forces heterogeneous governance arrangements into a single metric whose information compression destroys context-specific nuance. We propose translation-enhanced reform as the alternative, grounded in a Theoretical Climate Action Framework that identifies the CBAM failures as systematic deficits in cross-jurisdictional coordination, legitimacy through fair burden-sharing, and reflexive capacity to absorb lessons from alternative mechanisms. The translation approach is operationalizable within the existing CBAM legal architecture: Article 2(12) explicitly authorizes the Union to conclude agreements with third countries taking into account their carbon pricing mechanisms, Article 9(4) empowers the Commission to adopt implementing acts on carbon price conversion methodology, and the Article 30(2) review cycle provides an institutional pathway for incorporating pilot outcomes. A three-step pilot covering India, Brazil, and Turkey during 2026 through 2028 is proposed, with the objective of producing mature protocols in time for the Commission's default carbon price implementing act still pending adoption. CBAM may prevent carbon leakage. Whether it can sustain the international cooperation essential for global climate action depends on reforms that the present policy window remains open to, and that the window's accelerating closure makes increasingly urgent.

1. Introduction: The €90 Billion Question

On January 1, 2026, CBAM moved from reporting to payment. Importers of steel, aluminum, cement, fertilizers, hydrogen, and electricity must now purchase certificates linked to the EU Emissions Trading System, priced between €70 and €90 per tonne through the first quarter of 2026 [4]. The mechanism aims to level the playing field between EU producers bearing carbon costs and foreign producers who face no such constraints.

The numbers are substantial. Transitional period data covering 2023 and 2024 shows CBAM-covered imports totaling approximately €89 billion, with embedded emissions estimated at 260 million tonnes CO₂ equivalent [5]. These figures use CIF valuation for trade and include direct production emissions plus upstream electricity for covered products. Steel accounts for 69 percent of physical volume, fertilizers 15 percent, cement 11 percent. Aluminum, despite only 5 percent by weight, contributes 24 percent of embedded emissions, a reflection of primary smelting's extraordinary energy intensity [6]. By 2030, when free allowances fall to 48.5 percent, CBAM could generate €9 billion annually. By 2034, the steel sector alone could face over €30 billion in annual payments.

A critical distinction must be made at the outset. CBAM has a narrow legal objective: preventing carbon leakage and maintaining EU ETS integrity. It also carries a broader legitimacy claim, which is the assertion that it represents a fair contribution to global decarbonization. These are different standards. CBAM can succeed on the first while failing on the second. The four blind spots identified here concern the legitimacy dimension. We do not question whether CBAM will prevent leakage. We question whether the mechanism, as currently designed, can sustain international cooperation essential for addressing climate change at global scale.

Article 9 of the CBAM Regulation permits deduction of carbon costs "effectively paid in any form" in the country of origin [7]. The Commission reads this narrowly: only explicit carbon taxes and ETS payments qualify, and the qualification is further conditioned on cash actually having changed hands rather than on any broader concept of carbon-related economic burden. This interpretation excludes three distinct categories of cost that exporting countries have accumulated through alternative instruments, and the resulting framework carries four structural blind spots. The problem is not marginal. It is architectural.

The analysis that follows draws on the Theoretical Climate Action Framework (TCAF) developed in earlier TTI work [8]. Derived from cybernetic first principles, TCAF identifies six necessary functions of climate governance: boundary perception (Q1), autonomy-supervision balance (Q2), coordination (Q3), adaptive intelligence (Q4), policy coherence and legitimacy (Q5), and reflexive learning (Q6). The four blind spots identified below correspond to systematic deficits in how CBAM's current design addresses three of these functions, particularly Q3 coordination across jurisdictions, Q5 legitimacy through fair burden-sharing, and Q6 reflexive capacity to learn from diverse governance experiences. Section 7 develops this framing in detail.

Remaining content is for members only.

Please become a free member to unlock this article and more content.

Subscribe NowAuthor

Alex is the founder of the Terawatt Times Institute, developing cognitive-structural frameworks for AI, energy transitions, and societal change. His work examines how emerging technologies reshape political behavior and civilizational stability.