CBAM Country Intelligence Mexico 2026: Mid-Transition Reverse Penalty Risk from Concave Benchmark Coverage and Carbon Price Penetration Failure

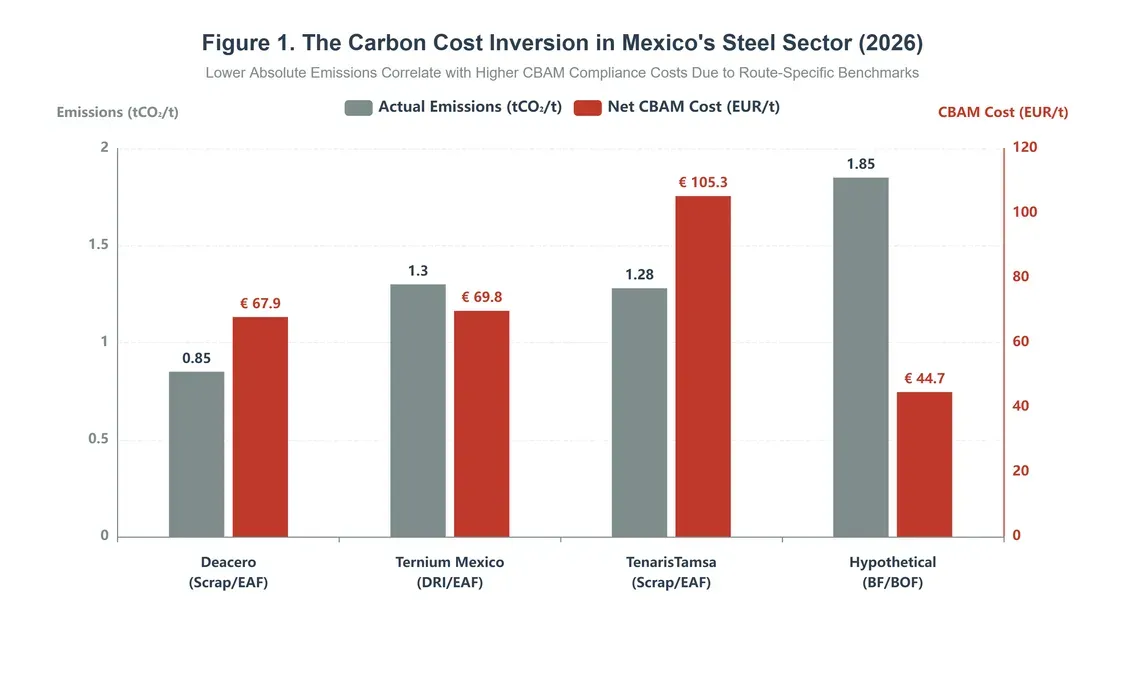

Mexico's 97%-recycled steel pays more CBAM than hypothetical blast furnaces. TTI Vol.13 models four facilities under Reg 2025/2620 benchmarks: Deacero €67.9/t, TenarisTamsa €105.3/t, hypothetical BF €44.7/t. The mid-transition reverse penalty concentrates in 2026–2030.

Executive Summary

Mexico's steel sector presents a paradox that aggregate trade statistics cannot capture. Mexican steel exports to the European Union total EUR 56 million annually, amounting to 0.02 percent of GDP. The sector runs 93 to 100 percent on electric arc furnaces. Deacero, the country's largest long-products manufacturer, recycles 97 percent of its metallic input. By every conventional measure of Carbon Border Adjustment Mechanism (CBAM) exposure, Mexico should rank among the least affected developing economies.

Facility-level arithmetic inverts this narrative. When the route-specific benchmarks published under Implementing Regulation (EU) 2025/2620 are applied to actual Mexican emission profiles, the firm with the lowest absolute emissions pays the most per tonne exported. Deacero faces a net CBAM compliance cost of EUR 67.9 per tonne of hot-rolled product in 2026. Ternium Mexico, operating a natural-gas-based direct reduction route at materially higher emissions, faces a comparable or even lower cost of EUR 51.8 to 69.8 depending on state-level carbon tax access. TenarisTamsa confronts EUR 105.3 per tonne on its seamless pipe exports. A hypothetical blast furnace operator would pay only EUR 44.7 per tonne.

This report identifies the structural phenomenon driving the inversion as mid-transition reverse penalty risk. CBAM's benchmark architecture assigns each production technology its own yardstick calibrated to European best practice within that lane. Scrap-based EAF receives a benchmark of 0.072 tCO₂ per tonne, shielding only 8 percent of Deacero's embedded emissions after the 2026 phase-in. Blast furnaces receive 1.370, shielding 72 percent. The industry that has exited the protected lane but has not reached the European frontier within the new lane absorbs the heaviest relative burden. Mexico sits at the deepest point of this concavity.

Five institutional dimensions converge simultaneously. Industrial structure has shifted almost entirely to electric steelmaking. The federal carbon tax exempts natural gas, reducing the penetrated effective rate to USD 2.1 per tonne of CO₂, covering 2.2 percent of the EU Emissions Trading System price. National carbon data infrastructure lacks product-level granularity. No federal CBAM coordination mechanism has been established. Trade volumes stay below macro-level visibility but concentrate in products acutely sensitive to per-tonne surcharges.

The reverse penalty concentrates in the 2026 to 2030 phase-in window, coinciding with the period during which Mexican exporters must commit to foundational infrastructure investments. Distorted cost signals during this window risk producing path dependencies that outlast the distortion itself. The report quantifies three enterprise-level financial options, the fiscal arithmetic of a federal natural gas carbon tax, state-level carbon tax design implications under Article 9, and credit risk dimensions for nearshoring project finance.

1. The Paradox of Transition

1.1 A Counterintuitive Finding

Every macroeconomic indicator points in the same direction. Mexico's steel exports to the European Union totaled EUR 56 million in 2024, amounting to 0.02 percent of the country's gross domestic product [1][2]. The national steel sector runs almost entirely on electric arc furnaces, a technology family that the European Commission itself has placed at the center of its industrial decarbonization strategy [3]. Deacero, the largest Mexican producer of long steel products, recycles 97 percent of its metallic input and reports the lowest CO₂ emission rate per tonne in North America [4]. By any conventional measure of exposure to the EU's Carbon Border Adjustment Mechanism (CBAM), Mexico should rank among the least affected developing economies.

Facility-level arithmetic inverts this narrative. When the route-specific CBAM benchmarks published under Implementing Regulation (EU) 2025/2620 on December 22, 2025, are applied to the actual emission profiles of Mexico's principal steelmakers, a pattern emerges that no aggregate trade statistic can capture [5]. Deacero faces a net CBAM compliance cost of EUR 67.9 per tonne of hot-rolled product in 2026. Ternium Mexico, operating a natural-gas-based direct reduction and electric arc furnace (DRI-EAF) route at materially higher absolute emissions, faces a comparable or even lower net cost of EUR 51.8 to 69.8, depending on the effective state carbon tax deduction available in its home state of Nuevo León. TenarisTamsa, Mexico's largest steel exporter to the EU by value, confronts EUR 105 per tonne on its seamless pipe products. A hypothetical blast furnace operator exporting the same product type would pay only EUR 44.7 before any domestic deduction.

The firm with the lowest emissions pays the most. The firm with the highest pays the least.

Each production route receives a separate benchmark yardstick calibrated to the top performers among European facilities operating that same route [5][6]. The blast furnace route carries a benchmark of 1.370 tonnes of CO₂ per tonne of product, shielding 74 percent of a typical operator's emissions. The scrap-based EAF route carries 0.072, shielding just 8 percent of Deacero's reported emissions and only 5.6 percent of TenarisTamsa's. What determines the level of protection is not how clean a producer is in absolute terms, but how close it sits to the European frontier within its own technological lane. Mexico's steelmakers are clean by global standards. They are far from the European top decile within the lanes they occupy.

Mexico's penetrated effective carbon price deepens the asymmetry. The federal carbon tax under the Ley del Impuesto Especial sobre Producción y Servicios (IEPS) exempts natural gas from its taxable base entirely, which means that the single largest emission source in DRI steelmaking carries a federal carbon price of precisely zero [7][8]. State-level carbon taxes exist in several jurisdictions but are either absent in key steelmaking states such as Coahuila and Veracruz, or subject to regressive tiering that reduces the effective rate for large emitters to as little as 7 percent of the statutory level [9]. When these layers are combined, the weighted-average effective carbon price across a representative DRI-EAF facility amounts to USD 2.1 per tonne of CO₂. Against the EU ETS allowance price of EUR 87 in early 2026 [10], this covers 2.2 percent. The Article 9 carbon price deduction available to Mexican exporters under Regulation (EU) 2023/956 is correspondingly negligible [11].

1.2 Mid-Transition Reverse Penalty Risk

These findings point to a structural phenomenon that this report terms mid-transition reverse penalty risk. An industry that has completed a first transition phase, moving from blast furnaces to electric arc furnaces or from coal to natural gas, has left the technological lane where CBAM provides the most generous protection. Yet it has not reached the European frontier where protection becomes unnecessary because actual emissions fall below the CBAM benchmark for electric arc furnace steel. The middle of the transition is the most expensive place to be, and the penalty concentrates precisely there.

Mexico is the first country in this series where the mid-transition condition manifests simultaneously across five institutional dimensions. In industrial structure, 93 to 100 percent of crude steel capacity has shifted to electric arc furnaces, exiting the protected BF/BOF lane for the thinly protected EAF lanes [12][13]. In carbon pricing, federal and state instruments exist but deliver an effective rate covering 2.2 percent of the EU benchmark [7][8][9]. In data infrastructure, a national emissions registry operates but lacks the product-level granularity that CBAM reporting requires [14]. In policy response, the government maintains climate commitments and a comprehensive industrial strategy but has established no federal CBAM coordination mechanism [15][16]. In trade composition, EU-bound volume is too small for macro-level alarm but concentrated in products where per-tonne margins are acutely sensitive to carbon border adjustment surcharges [2].

The reverse penalty is strongest during the 2026 to 2030 CBAM phase-in period, when the Specific Embedded Free Allocation (SEFA) still provides partial but shrinking benchmark protection. SEFA is the per-tonne emission quantity shielded from CBAM certificate obligations, calculated as the route-specific benchmark multiplied by a factor reflecting remaining EU ETS free allocation. Think of it as a tax-free allowance on carbon "income": the allowance shrinks each year as the phase-in factor φ increases from 0.025 in 2026 toward 1.0 in 2034, at which point all benchmark protection vanishes and absolute emissions alone determine cost [5][11]. After 2034, a facility emitting 1.30 tCO₂/t will pay more than one emitting 0.85, regardless of route. The reverse penalty is a window-period phenomenon governing CBAM's first eight years. Those years coincide with the period in which Mexican exporters must make foundational investment decisions about monitoring infrastructure, verification partnerships, and feedstock strategy. Distorted cost signals during this window may lock in suboptimal decisions that persist well beyond the window itself.

1.3 Positioning This Report

This analysis differs from existing CBAM impact assessments for developing countries in three respects. Instead of national aggregates, this report takes the individual facility as its unit of analysis: where aggregate studies report a GDP share of 0.02 percent [1], this report calculates the CBAM compliance cost per tonne for each principal exporter using disclosed Scope 1 emission intensities and legally binding benchmarks [5]. The Article 9 carbon price deduction is computed from penetrated effective rates, not statutory rates, surviving federal fuel exemptions, state tiering, and constitutional litigation risk [7][8][9]. A third distinguishing feature is the treatment of the product boundary between the CBAM benchmark (terminating at continuous casting per Delegated Regulation (EU) 2019/331 [17]) and the CBAM declaration (extending to the finished product per Implementing Regulation (EU) 2025/2547 [18]) as a quantified financial variable rather than a footnote.

Remaining content is for paid members only.

Please subscribe to any paid plan to unlock this article and more content.

Subscribe Now